What Lies Ahead for Network Tokenisation as Global Adoption Shows an Upward Trend?

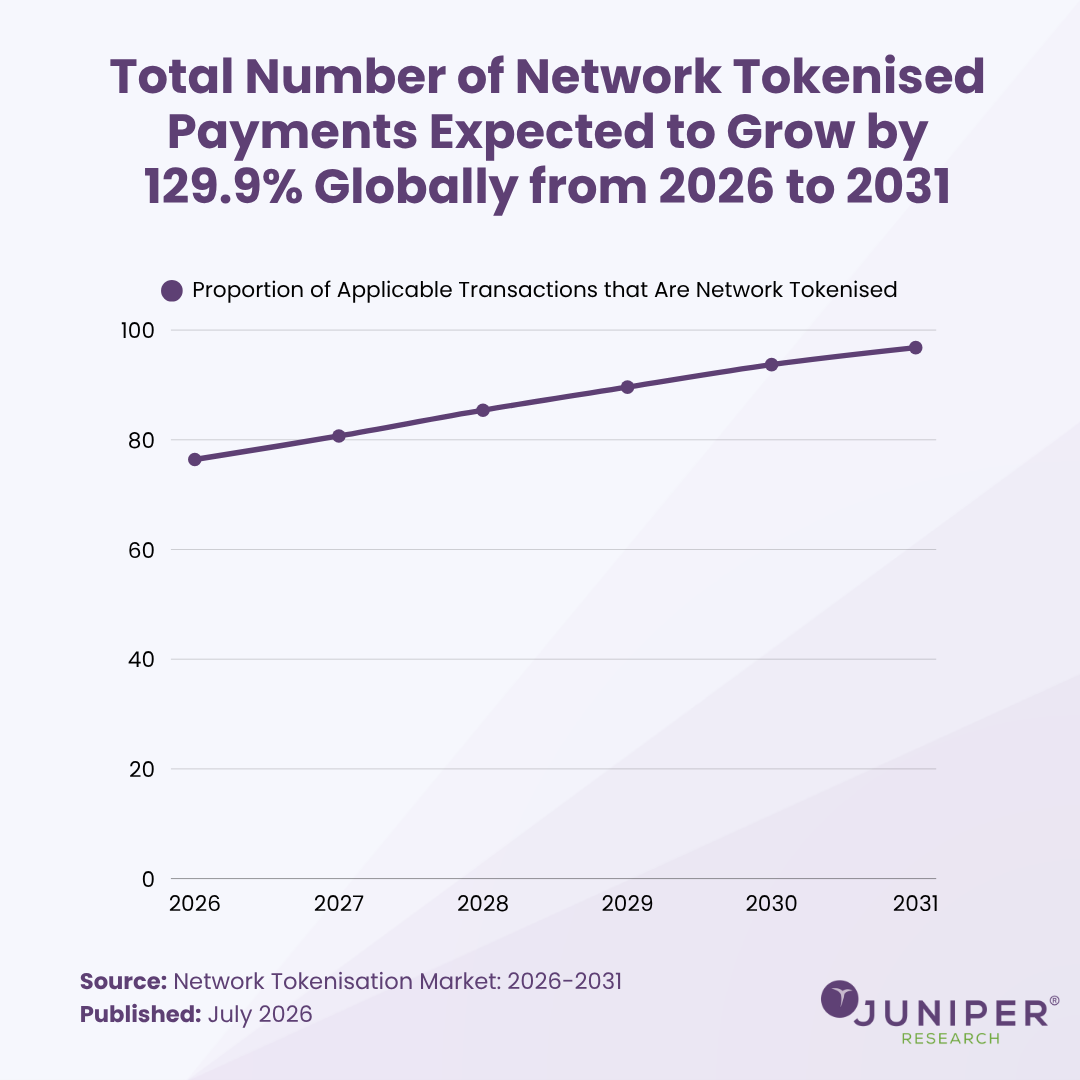

Network tokenisation continues to grow as the market moves from early adoption to broad operational necessity. Our latest research indicates global penetration rises from 76.4% in 2026 to 96.8% by 2031; suggesting that the technology is becoming close to standard infrastructure, rather than a niche enhancement. This trajectory is consistent with wider industry adoption drivers such as better authorisation rates, lower fraud, reduced churn in recurring payments and improved checkout conversion; all of which make network tokenisation commercially hard to ignore.

What’s Driving Adoption?

The Visa and Mastercard 2030 mandates create a strong gravitational pull towards network token adoption across the payments’ ecosystem. In practical terms, they encourage issuers, acquirers, PSPs and merchants to support tokenised credentials at scale, which pushes the market from optional adoption to expected capability. This will accelerate investment, product roadmaps, and integration work well beyond the card schemes themselves, because vendors that are not ready, risk being left behind as token-enabled acceptance becomes the norm.

The effect is global, not just scheme-specific, as the mandates influence markets that may not be directly governed by Visa or Mastercard rules, but still depend on their reach for cross-border commerce, digital wallets and recurring card payments. Even where domestic schemes dominate locally, international merchants and PSPs will increasingly require token support to preserve conversion and continuity across geographies. As a result, the 2030 mandates are likely to set a de facto standard that shapes the behaviour of payment providers in Europe, APAC, Latin America and other regions with strong card-not-present growth.

Broader Ramifications for Providers

For providers, network tokenisation has strategic implications that extend well beyond fraud reduction, as it is becoming a core enabler of higher authorisation rates, lower churn in recurring payments, and improved checkout performance across digital commerce. Providers that position tokenisation as a standalone security layer risk competing on a narrow feature set, whereas those that embed it into broader value-added services, such as lifecycle management, orchestration, retries, reporting and scheme optimisation, can create stronger merchant stickiness and more defensible revenue. It also raises the bar on partnerships, as providers need to align with global card schemes, domestic schemes, and wallet ecosystems to stay relevant across regions.

The Bigger Picture

The broader takeaway is that network tokenisation is no longer just following payments growth; it is increasingly helping shape it. The significant forecast rise suggests a market approaching saturation in the best sense - adoption becomes so widespread that tokenisation is simply part of how digital payments work. Vendors that want to capitalise should therefore move quickly on local scheme partnerships, recurring-payment optimisation, merchant performance dashboards, and market-specific propositions that turn compliance pressure into commercial advantage.

Source: Network Tokenisation Market: 2026-2031

Read the Press Release: Network Tokenisation to Secure 2.4 Trillion Global Transactions Between 2026 and 2030 – Representing 86% of Applicable Transactions

Download the Whitepaper: The Top Three Drivers of Network Tokenisation Adoption

Latest research, whitepapers & press releases

-

ReportJuly 2026Fintech & Payments

ReportJuly 2026Fintech & Payments Shane O'SullivanDigital Travel Credential Market: 2026-2035

Shane O'SullivanDigital Travel Credential Market: 2026-2035Our Digital Travel Credential Market research suite provides detailed analysis of this rapidly changing market; allowing digital travel credential solution providers, regulatory bodies, border control authorities, airlines, and airport operators to gain a comprehensive understanding of key digital travel trends, implementation challenges, future growth opportunities, and the competitive environment.

VIEW -

ReportJuly 2026Fintech & Payments

ReportJuly 2026Fintech & Payments Thomas WilsonNetwork Tokenisation Market: 2026-2031

Thomas WilsonNetwork Tokenisation Market: 2026-2031Our Network Tokenisation research suite provides a comprehensive and in-depth analysis of the ecosystem surrounding network tokenisation, enabling stakeholders such as merchants, payment gateways, token service providers and token requestors to understand future growth, key trends and the competitive environment.

VIEW -

ReportJuly 2026Telecoms & Connectivity

ReportJuly 2026Telecoms & Connectivity Alex WebbSponsored Roaming Competitor Leaderboard: 2026

Alex WebbSponsored Roaming Competitor Leaderboard: 2026Our Sponsored Roaming Competitor Leaderboard 2026 delivers competitor benchmarking and analysis of 14 leading sponsored roaming vendors.

VIEW -

ReportJune 2026Telecoms & Connectivity

ReportJune 2026Telecoms & Connectivity Ardit BallhysaRAN Vendors Competitor Leaderboard: 2026

Ardit BallhysaRAN Vendors Competitor Leaderboard: 2026Our Radio Access Network (RAN) Vendor Competitor Leaderboard provides insightful analysis of a market that is experiencing significant change currently, and will continue to do so over the next five years.

VIEW -

ReportJune 2026Fintech & Payments

ReportJune 2026Fintech & Payments Michael GreenwoodChargeback Management Market: 2026-2031

Michael GreenwoodChargeback Management Market: 2026-2031Our Chargeback Management research suite provides detailed analysis of this fast-changing market; allowing chargeback management providers to gain an understanding of key payment trends and challenges, potential growth opportunities, and the competitive environment.

VIEW -

ReportJune 2026Telecoms & Connectivity

ReportJune 2026Telecoms & Connectivity Peter BoylandConversational AI Market: 2026-2030

Peter BoylandConversational AI Market: 2026-2030Our Conversational AI Market 2026-2030 research suite provides insightful analysis of a market that will experience significant growth in the next five years.

VIEW

-

WhitepaperJuly 2026Fintech & Payments

Thomas Wilson

WhitepaperJuly 2026Fintech & Payments

Thomas WilsonThe Top Three Drivers of Network Tokenisation Adoption

Our complimentary whitepaper, The Top Three Drivers of Network Tokenisation Adoption, examines the state of the network tokenisation market; considering its impact on different payment modalities, how it is shaping the modern payments landscape through safer, more secure payments, and how it could unlock the potential of agentic commerce.

VIEW -

WhitepaperJune 2026Fintech & Payments

WhitepaperJune 2026Fintech & Payments Nick Maynard

Nick MaynardMoney20/20 Europe 2026 Key Takeaways: What You Need to Know Post-event

Money 20/20 Europe once again brought together people from across the fintech, payments and identity ecosystems; creating three days of discussions, announcements and networking.

VIEW -

WhitepaperJune 2026Fintech & Payments

Michael Greenwood

WhitepaperJune 2026Fintech & Payments

Michael GreenwoodChargeback Management: The Fightback Against Friendly Fraud

Our complimentary whitepaper, Chargeback Management: The Fightback Against Friendly Fraud, examines the growing impact of friendly fraud on the chargeback management space, as well as how chargeback management tools are mitigating this threat.

VIEW -

WhitepaperJune 2026Telecoms & Connectivity

Peter Boyland

WhitepaperJune 2026Telecoms & Connectivity

Peter BoylandAgentic and Conversational AI: Streamlining Revenue Opportunities

Our complimentary whitepaper, Agentic and Conversational AI: Streamlining Revenue Opportunities, explores the challenges and opportunities for operators and enterprises as conversational AI becomes more embedded in the consumer experience.

VIEW -

WhitepaperJune 2026Telecoms & Connectivity

Alex Webb

WhitepaperJune 2026Telecoms & Connectivity

Alex WebbNo Tower? No Problem: How Direct to Cell is Rewriting the Rules of Connectivity

Our complimentary whitepaper explores consumer demand for direct to cell services and provides strategic recommendations for how MNOs can optimise these services.

VIEW -

WhitepaperMay 2026Telecoms & Connectivity

Alex Webb

WhitepaperMay 2026Telecoms & Connectivity

Alex WebbLearning from 5G - How MNOs Can Make 6G a Success

Our complimentary whitepaper, Learning from 5G - How MNOs Can Make 6G a Success, explores the lessons that mobile network operators can learn from the development and commercialisation of 5G and apply to 6G.

VIEW

-

Fintech & Payments

Network Tokenisation to Secure 2.4 Trillion Global Transactions Between 2026 and 2030 – Representing 86% of Applicable Transactions

July 2026 -

Telecoms & Connectivity

Juniper Research Identifies BICS, Telna, and Vodafone Procure & Connect as Leaders in the Sponsored Roaming Market

July 2026 -

Fintech & Payments

Digital Identity Verification Checks to Reach 175 Billion Globally by 2030, with Biometric Verification the Fastest-growing Modality

July 2026 -

Fintech & Payments

Agentic Commerce to Reach 1.3 Billion Users Globally by 2031, as Card Infrastructure Leads the Way

June 2026 -

Fintech & Payments

Juniper Research Unveils Fintech & Payments Awards Winners for 2026

June 2026 -

Fintech & Payments

Consumer Payments Predictions 2026/27: Market Driven by Agentic Commerce, Bank-backed Wallets, & Click to Pay

June 2026