SpaceX’s IPO Setting the Standard for Terrestrial Telcos

SpaceX filed its S-1 with the Securities and Exchange Commission (SEC) on 20 May 2026, and coverage of the event has largely converged on the same points: the largest listing in history, a reported valuation of $1.75 trillion-$2 trillion, Musk's 85% voting control, and xAI's losses at group level. The figure that is particularly interesting, from a connectivity perspective, appears further into the prospectus. In 2025, the Connectivity segment, primarily Starlink, recorded $11.39 billion in revenue, up 50% year-on-year, with operating profit of $4.42 billion and adjusted EBITDA of $7.17 billion; a 63% margin. For terrestrial mobile operators, SpaceX’s initial public offering (IPO) sets a new precedent for what is possible, with Starlink proving that satellite connectivity can be both highly profitable and competitive against terrestrial networks.

Starlink Is the Business Actually Being Listed

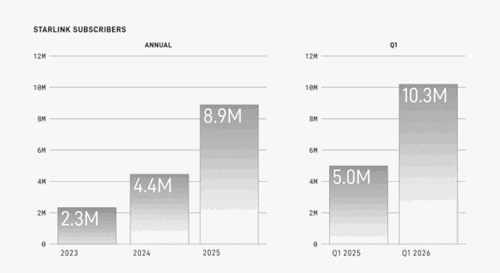

When reading the SpaceX prospectus, it is easy to get lost in the Mars rhetoric and the rocket photography; however, what becomes clear is that the cash engine inside SpaceX is a broadband operator. The connectivity segment covers SpaceX's Starlink services and accounts for the majority of the company's revenue and earnings - $11.4 billion in 2025 and $3.3 billion in the first quarter of 2026, with adjusted EBITDA of $7.2 billion in 2025 and $2.1 billion in the first quarter. Connectivity accounted for roughly 61% of overall company revenue in 2025, which includes the merged SpaceX, Starlink, and xAI entities. The subscriber base has reached scale fast: as of 31 March 2026, Starlink had 10.3 million subscribers across 164 countries and territories.

Figure 1: Starlink Subscribers

Source: SpaceX SEC Filing

Whilst it is reported that Starlink’s average monthly revenue per subscriber fell from $99 in 2023 to $66 in the first quarter of 2026, the strategy is clear: Starlink is trading volume for reach. To expand into lower-income markets, such as large parts of Africa, South Asia, and Latin America, Starlink cannot charge what it charges in Western markets. Instead, it offers cheaper tiers for access; therefore accepting a lower revenue per customer in exchange for more customers across more of the world. The 63% segment EBITDA margin is what makes this possible – and has been achieved without traditional infrastructure such as copper, fibre, or tower portfolio to maintain. This provides SpaceX a structurally different cost base from any operator.

The IPO Sets a Precedent

Before this filing, there had been no clean, public comparable for satellite broadband. Viasat and EchoStar are legacy businesses carrying heavy debt, with broadband as one line among several declining ones. Eutelsat OneWeb, the nearest equivalent, is a blended geostationary orbit (GEO) and Low Earth Orbit (LEO) operator, listed in Paris, with state involvement in its ownership and a weak market valuation. Not one of these three businesses provides a clean valuation for LEO broadband economics on their own terms. The SpaceX prospectus changes this. Its segment disclosure, combined with a daily trading price once SPCX lists on Nasdaq, gives the market far better material to value a satellite-broadband operator running a 63% segment margin and 50% revenue growth.

The benchmark SpaceX is setting illustrates the ruthlessness in economic efficiency, compared to incumbent mobile network operators (MNOs) running structurally lower margins alongside continuous capital expenditure commitment. Furthermore, with fibre build-out, 5G densification, and 6G investment in view, MNOs cannot avoid this spending without conceding competitive ground.

The EchoStar Spectrum Gives Starlink Options

Largely, Starlink’s direct to device (D2D) business is seen as a coverage-extension layer sold through mobile partners such as T-Mobile in the United States, Optus and Telstra in Australia, Rogers in Canada, and KDDI in Japan. So much so, that the framing assumes the satellite operator depends on the carrier, because the carrier supplies the licensed spectrum on which the service runs.

However, in September 2025, SpaceX agreed to buy EchoStar’s AWS-4 and H-block spectrum licences for approximately $17 billion, split between up to $8.5 billion in cash and up to $8.5 billion in stock. In November, it added EchoStar’s unpaired AWS-3 licences for roughly $2.6 billion in stock. Owning licensed terrestrial spectrum gives Starlink a route to offering D2D service without an MNO partner’s spectrum at all; with SpaceX stating that the next generation of direct to cell (D2C) satellites will be designed to use this spectrum.

This IPO funds that next-generation constellation, and that creates an awkward position for the carriers currently treated as Starlink's distribution partners. Their own subscribers' D2D usage helps pay for the build-out of a system that could eventually compete with them directly.

What This Means for Operators

The newly acquired spectrum is not compatible with the current D2D satellites; the next-generation D2C satellites still have to be designed and deployed to use it, with the constellation not expected to be operational before roughly 2027. Satellite D2D capacity per cell remains far below that which a terrestrial macro site delivers, which limits it to messaging and narrowband use rather than mass mobile broadband. Usage data, so far, points to demand that is concentrated and intermittent - useful in dead zones and during emergencies, but not a wholesale replacement for the terrestrial network. There is also a question over the economics. Starlink's model trades average revenue per user (ARPU) for scale: revenue per subscriber has fallen sharply while the subscriber count has grown faster; keeping total revenue rising. That holds only as long as subscriber growth continues to outpace both ARPU compression and operating cost. If growth slows while ARPU keeps falling, the segment economics that make the comparison with terrestrial operators so stark would weaken.

An important caveat is that terrestrial telcos are not about to be made obsolete. What has shifted is the direction of travel and the balance of power, and that is what operators should price in. The response is not to worry over coverage maps; it is to treat the prospectus as a competitive document. Operators should reassess D2D partnership terms before the next-generation constellation flies, and specifically test whether a multi-year wholesale arrangement signed today funds a future competitor. They should watch the Federal Communications Commission’s (FCC's) AWS-3 auction, where SpaceX has already signalled appetite for more terrestrial spectrum, and expect their own investors to raise the margin comparison once SPCX has a trading history. Juniper Research expects satellite D2D to move from a coverage footnote to a board-level question for MNOs within the next two to three years.

---

i: https://www.sec.gov/Archives/edgar/data/1181412/000162828026036936/spaceexplorationtechnologi.htm#id286866c4c474ba490d6531a57db9e93_60

Related Research

-

ReportJune 2026Telecoms & Connectivity

ReportJune 2026Telecoms & Connectivity Alex WebbDirect to Cell Market, 2026-2031

Alex WebbDirect to Cell Market, 2026-2031Our newest Direct-to-Cell research provides market stakeholders, such as mobile network operators and satellite network operators, with key analysis of the future of this rapidly emerging market.

VIEW -

ReportOctober 2025IoT & Emerging Technology

Alex WebbDirect to Satellite Market, 2025-2030

ReportOctober 2025IoT & Emerging Technology

Alex WebbDirect to Satellite Market, 2025-2030Juniper Research’s Direct to Satellite research suite provides satellite providers, investors, and partners, such as Mobile Network Operators, with an extensive analysis and insights into the direct to satellite market.

VIEW

Latest research, whitepapers & press releases

-

ReportJuly 2026Fintech & Payments

ReportJuly 2026Fintech & Payments Jawad JahanPOS Market: 2026-2031

Jawad JahanPOS Market: 2026-2031Our Point of Sale (POS) Market research suite provides detailed and insightful analysis of this evolving market; enabling stakeholders - from POS hardware manufacturers, payment infrastructure providers, software developers, and hospitality and retail vendors - to understand future growth, key trends, and the competitive environment.

VIEW -

ReportJuly 2026Fintech & Payments

ReportJuly 2026Fintech & Payments Shane O'SullivanDigital Travel Credential Market: 2026-2035

Shane O'SullivanDigital Travel Credential Market: 2026-2035Our Digital Travel Credential Market research suite provides detailed analysis of this rapidly changing market; allowing digital travel credential solution providers, regulatory bodies, border control authorities, airlines, and airport operators to gain a comprehensive understanding of key digital travel trends, implementation challenges, future growth opportunities, and the competitive environment.

VIEW -

ReportJuly 2026Fintech & Payments

ReportJuly 2026Fintech & Payments Thomas WilsonNetwork Tokenisation Market: 2026-2031

Thomas WilsonNetwork Tokenisation Market: 2026-2031Our Network Tokenisation research suite provides a comprehensive and in-depth analysis of the ecosystem surrounding network tokenisation, enabling stakeholders such as merchants, payment gateways, token service providers and token requestors to understand future growth, key trends and the competitive environment.

VIEW -

ReportJuly 2026Telecoms & Connectivity

ReportJuly 2026Telecoms & Connectivity Alex WebbSponsored Roaming Competitor Leaderboard: 2026

Alex WebbSponsored Roaming Competitor Leaderboard: 2026Our Sponsored Roaming Competitor Leaderboard 2026 delivers competitor benchmarking and analysis of 14 leading sponsored roaming vendors.

VIEW -

ReportJune 2026Telecoms & Connectivity

ReportJune 2026Telecoms & Connectivity Ardit BallhysaRAN Vendors Competitor Leaderboard: 2026

Ardit BallhysaRAN Vendors Competitor Leaderboard: 2026Our Radio Access Network (RAN) Vendor Competitor Leaderboard provides insightful analysis of a market that is experiencing significant change currently, and will continue to do so over the next five years.

VIEW -

ReportJune 2026Fintech & Payments

ReportJune 2026Fintech & Payments Michael GreenwoodChargeback Management Market: 2026-2031

Michael GreenwoodChargeback Management Market: 2026-2031Our Chargeback Management research suite provides detailed analysis of this fast-changing market; allowing chargeback management providers to gain an understanding of key payment trends and challenges, potential growth opportunities, and the competitive environment.

VIEW

-

WhitepaperJuly 2026Fintech & Payments

Shane O'Sullivan

WhitepaperJuly 2026Fintech & Payments

Shane O'SullivanBeyond the Boarding Pass: The Digital Travel Credential Paradigm

Our complimentary whitepaper, Beyond the Boarding Pass: The Digital Travel Credential Paradigm, examines the rapidly evolving state of the digital travel credential market.

VIEW -

WhitepaperJuly 2026Fintech & Payments

Thomas Wilson

WhitepaperJuly 2026Fintech & Payments

Thomas WilsonThe Top Three Drivers of Network Tokenisation Adoption

Our complimentary whitepaper, The Top Three Drivers of Network Tokenisation Adoption, examines the state of the network tokenisation market; considering its impact on different payment modalities, how it is shaping the modern payments landscape through safer, more secure payments, and how it could unlock the potential of agentic commerce.

VIEW -

WhitepaperJune 2026Fintech & Payments

WhitepaperJune 2026Fintech & Payments Nick Maynard

Nick MaynardMoney20/20 Europe 2026 Key Takeaways: What You Need to Know Post-event

Money 20/20 Europe once again brought together people from across the fintech, payments and identity ecosystems; creating three days of discussions, announcements and networking.

VIEW -

WhitepaperJune 2026Fintech & Payments

Michael Greenwood

WhitepaperJune 2026Fintech & Payments

Michael GreenwoodChargeback Management: The Fightback Against Friendly Fraud

Our complimentary whitepaper, Chargeback Management: The Fightback Against Friendly Fraud, examines the growing impact of friendly fraud on the chargeback management space, as well as how chargeback management tools are mitigating this threat.

VIEW -

WhitepaperJune 2026Telecoms & Connectivity

WhitepaperJune 2026Telecoms & Connectivity Peter Boyland

Peter BoylandAgentic and Conversational AI: Streamlining Revenue Opportunities

Our complimentary whitepaper, Agentic and Conversational AI: Streamlining Revenue Opportunities, explores the challenges and opportunities for operators and enterprises as conversational AI becomes more embedded in the consumer experience.

VIEW -

WhitepaperJune 2026Telecoms & Connectivity

Alex Webb

WhitepaperJune 2026Telecoms & Connectivity

Alex WebbNo Tower? No Problem: How Direct to Cell is Rewriting the Rules of Connectivity

Our complimentary whitepaper explores consumer demand for direct to cell services and provides strategic recommendations for how MNOs can optimise these services.

VIEW

-

Fintech & Payments

Digital Travel Credentials: 1.2 Billion Passengers to Adopt DTCs Globally by 2035, Fuelled by Passenger Demand for Seamless Journeys

July 2026 -

Fintech & Payments

Network Tokenisation to Secure 2.4 Trillion Global Transactions Between 2026 and 2030 – Representing 86% of Applicable Transactions

July 2026 -

Telecoms & Connectivity

Juniper Research Identifies BICS, Telna, and Vodafone Procure & Connect as Leaders in the Sponsored Roaming Market

July 2026 -

Fintech & Payments

Digital Identity Verification Checks to Reach 175 Billion Globally by 2030, with Biometric Verification the Fastest-growing Modality

July 2026 -

Fintech & Payments

Agentic Commerce to Reach 1.3 Billion Users Globally by 2031, as Card Infrastructure Leads the Way

June 2026 -

Fintech & Payments

Juniper Research Unveils Fintech & Payments Awards Winners for 2026

June 2026