Circle, Fireblocks, SWIFT and the Race to Rewire Cross-border Payments

Wiring money internationally has always been met with the same frustrations, such as multi-day waits, fees that seems to multiply with every bank that touches the transaction, and no clear way to track where your money actually is. In a nutshell, this is the reality of SWIFT - the messaging network that has connected the world’s banks since 1973. The SWIFT network is still used for the vast majority of global cross-border payments, and for decades it was the only real player in town. However, this status quo is now being challenged.

Two companies in particular have made it clear they want to change how money moves across borders. Circle Internet Group - the company behind the stablecoin, USD Coin (USDC), and Fireblocks, a major institutional digital asset platform. In April 2025, Circle launched its Circle Payments Network (CPN), whilst Fireblocks unveiled its own Fireblocks Network for Payments, in September 2025. Both are effectively building what is being described as ‘SWIFT for stablecoins’.

What SWIFT Doesn’t Do

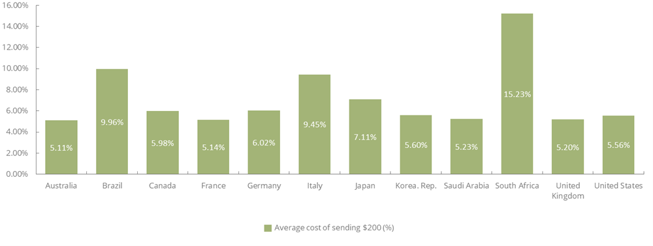

SWIFT does not move money. It moves messages about money. So, when a bank sends a SWIFT payment, it is actually sending an instruction that must pass through a chain of correspondent banks; each reconciling their own accounts before passing the message along. The result is an international wire that can take anywhere from one to five business days and cost anywhere from 1% to 6% in fees, depending on the corridor. The World Bank reported that sending remittances costs an average of 6.49% of the amount sent, as of March 2025.

Average Cost of Sending from Select G20 Countries, as of Q3 2024

Source: World Bank

In many emerging markets, the drawdowns of traditional rails are pronounced, with correspondent banking relationships being less established and fees generally higher due to lower transaction volumes and weaker regulatory environments. Moreover, general de-risking since the post-2008 wave of anti-money laundering enforcement and bank fines has led to many Western banks cutting correspondent banking relationships in higher-risk regions.

Stablecoins, however, offer a fundamentally different approach. As a cryptocurrency pegged to the value of a traditional currency, such as the US dollar, stablecoins enable peer-to-peer settlement on a blockchain, where the transfer of value and the finality of the transaction happen simultaneously, without the need for intermediary banks. In the world of cryptocurrencies, transactions can settle in the matter of seconds, 24 hours a day, seven days a week, including bank holidays.

Two Networks, One Target

Circle’s CPN is explicitly designed to act as infrastructure for financial institutions to move money across borders using its flagship stablecoin products, such as the USDC or Euro Coin (EURC). With Banco Santander, Deutsche Bank, Société Générale, and Standard Chartered among its launch partners, the network now has 55 enrolled institutions, with a further 74 in the pipeline; generating $5.7 billion in annualised transaction volume. Similarly to SWIFT, CPN does not move funds itself. Instead, it acts as the coordination layer connecting participants and ensuring compliance and AML checks are built into every transaction flow.

On the other hand, Fireblocks is addressing the problem from a slightly different angle. Its payment network, launched in September 2025, connects over 40 providers including liquidity partners, on/off ramps, and stablecoin issuers (including Circle) across more than 100 countries and 60 currencies; handling approximately $200 billion in monthly stablecoin volume. Fireblocks is embedded directly in the movement, custody, and orchestration of assets, where its network sits at the execution layer. Whereas Circle’s CPN is designed to coordinate regulated financial institutions.

The institutional appetite for this is real. Fireblocks’ own State of Stablecoins 2025 report, based on a survey of over 300 payment providers and banks, found that 90% of financial institutions are either already using stablecoins or actively planning to. Nearly half cited cross-border payments as the primary use case, with speed the top-ranked benefit. In Latin America, this figure rises to 71%.

SWIFT Responds

Stablecoins and distributed ledgers have experienced significant growth and adoption as a tool for settlements over the years, and SWIFT has not stood still. At its annual Sibos conference, in September 2025, SWIFT announced that it was building a blockchain-based shared ledger in collaboration with over 30 global financial institutions, including Bank of America, JP Morgan Chase, HSBC, and BNP Paribas. The collaboration also involves Consensys; a leading blockchain software company focused on building infrastructure, developer tools, and decentralised applications for the Ethereum blockchain.

The ledger being built will use smart contracts to record, validate, and sequence transactions, and is designed to support stablecoins, tokenised deposits, and central bank digital currencies alongside traditional fiat. SWIFT also completed its migration to the ISO 20022 messaging standard, in November 2025, and, in December 2025, successfully completed a proof of concept with HSBC and Ant International for cross-border transfers of tokenised deposits.

Ultimately, the technology argument for stablecoins is largely won. Blockchain settlement is faster and cheaper than the correspondent banking model, and SWIFT knows it. But payments infrastructure is not just a technical problem; it is a trust and network problem. This is where SWIFT carries the competitive advantage. More than 11,000 financial institutions across 200 countries rely on SWIFT’s messaging service to securely communicate. Circle and Fireblocks, however compelling their propositions, are building those relationships from scratch.

Looking Ahead

In this landscape, there won’t be a clean winner, at least not any time soon. What is more likely, however, is a messy period where legacy rails and stablecoin networks run side by side, until the market gradually consolidates around whoever proves most reliable at scale.

SWIFT is not being replaced overnight. When a network has decades of experience and over 11,000 institutions on board, inertia alone buys some years to make up for complacency. However, as demonstrated by companies such as Circle and Fireblocks, moving fast is where SWIFT has been weak. The more interesting proposition is whether SWIFT is able to reinvent itself, or whether its blockchain efforts are ultimately a defensive play amidst the backdrop of rising competition.

Jawad is a Research Analyst at Juniper Research, specialising in financial technology and payments. He provides strategic analysis and actionable insights on the topics he covers, helping stakeholders stay ahead on emerging trends and shifting landscapes.

Latest research, whitepapers & press releases

-

ReportAugust 2026Fintech & Payments

ReportAugust 2026Fintech & Payments Nick MaynardContactless Payments Market Data: 2026-2031

Nick MaynardContactless Payments Market Data: 2026-2031Our Contactless Payments market analysis provides exhaustive data coverage of the market in its entirety, including the adoption of mobile wallets featuring contactless payment technology, the growth of contactless transactions, and the market’s associated values.

VIEW -

ReportAugust 2026Fintech & Payments

Nick MaynardDigital Ticketing Market Data: 2026-2031

ReportAugust 2026Fintech & Payments

Nick MaynardDigital Ticketing Market Data: 2026-2031Our Digital Ticketing report provides exhaustive coverage of the digital ticketing market, including the adoption rates of digital ticketing across different ticketing segments, as well as the use of wearable payments and chatbots.

VIEW -

ReportAugust 2026Fintech & Payments

Nick MaynardQR Code Payments Market: 2026-2031

ReportAugust 2026Fintech & Payments

Nick MaynardQR Code Payments Market: 2026-2031This research provides exhaustive coverage of the QR Code Payments market, including the adoption rates of QR code payment systems across retail, person-to-person (P2P), and ticketing use cases.

VIEW -

ReportJuly 2026IoT & Emerging Technology

ReportJuly 2026IoT & Emerging Technology Saffron DusanjhVLEO Satellite Market: 2026-2031

Saffron DusanjhVLEO Satellite Market: 2026-2031Our Very Low Earth Orbit (VLEO) Satellite Market research suite provides comprehensive analysis of one of the fastest-emerging markets within the global space economy.

VIEW -

ReportJuly 2026Telecoms & Connectivity

ReportJuly 2026Telecoms & Connectivity Alex WebbIPX Providers Competitor Leaderboard: 2026

Alex WebbIPX Providers Competitor Leaderboard: 2026Our IPX Providers Competitor Leaderboard 2026 delivers comprehensive evaluation and examination of 16 leading IPX vendors. It provides mobile network operators and other IPX customers with profiles, competitor benchmarking, and strategic analysis of these leading providers.

VIEW -

ReportJuly 2026Fintech & Payments

ReportJuly 2026Fintech & Payments Jawad JahanPOS Market: 2026-2031

Jawad JahanPOS Market: 2026-2031Our Point of Sale (POS) Market research suite provides detailed and insightful analysis of this evolving market; enabling stakeholders - from POS hardware manufacturers, payment infrastructure providers, software developers, and hospitality and retail vendors - to understand future growth, key trends, and the competitive environment.

VIEW

-

WhitepaperJuly 2026IoT & Emerging Technology

Saffron Dusanjh

WhitepaperJuly 2026IoT & Emerging Technology

Saffron DusanjhBeyond LEO: Why VLEO is Becoming the Next Growth Market

Our complimentary whitepaper, Beyond LEO: Why VLEO is Becoming the Next Growth Market, explores how VLEO is transitioning from an experimental orbital regime into a commercially viable market.

VIEW -

WhitepaperJuly 2026Fintech & Payments

Jawad Jahan

WhitepaperJuly 2026Fintech & Payments

Jawad JahanFrom Transaction to Transformation: The Future of POS

Our complimentary whitepaper, From Transaction to Transformation: The Future of POS, analyses the current landscape of the POS market. It also provides insight into key trends shaping the POS market, such as POS terminals increasingly being used as a business management platform.

VIEW -

WhitepaperJuly 2026Fintech & Payments

WhitepaperJuly 2026Fintech & Payments Shane O'Sullivan

Shane O'SullivanBeyond the Boarding Pass: The Digital Travel Credential Paradigm

Our complimentary whitepaper, Beyond the Boarding Pass: The Digital Travel Credential Paradigm, examines the rapidly evolving state of the digital travel credential market.

VIEW -

WhitepaperJuly 2026Fintech & Payments

WhitepaperJuly 2026Fintech & Payments Thomas Wilson

Thomas WilsonThe Top Three Drivers of Network Tokenisation Adoption

Our complimentary whitepaper, The Top Three Drivers of Network Tokenisation Adoption, examines the state of the network tokenisation market; considering its impact on different payment modalities, how it is shaping the modern payments landscape through safer, more secure payments, and how it could unlock the potential of agentic commerce.

VIEW -

WhitepaperJune 2026Fintech & Payments

Nick Maynard

WhitepaperJune 2026Fintech & Payments

Nick MaynardMoney20/20 Europe 2026 Key Takeaways: What You Need to Know Post-event

Money 20/20 Europe once again brought together people from across the fintech, payments and identity ecosystems; creating three days of discussions, announcements and networking.

VIEW -

WhitepaperJune 2026Fintech & Payments

WhitepaperJune 2026Fintech & Payments Michael Greenwood

Michael GreenwoodChargeback Management: The Fightback Against Friendly Fraud

Our complimentary whitepaper, Chargeback Management: The Fightback Against Friendly Fraud, examines the growing impact of friendly fraud on the chargeback management space, as well as how chargeback management tools are mitigating this threat.

VIEW

-

Fintech & Payments

Contact-free Payments Become the Default as Contactless Transactions Exceed $32 Trillion Globally by 2031

August 2026 -

IoT & Emerging Technology

VLEO Satellites: Global Investment to Near $10 Billion by 2031; Driven by Falling Launch Costs

July 2026 -

Telecoms & Connectivity

Juniper Research Identifies Syniverse, BICS, and iBASIS as Leaders in the IPX Market

July 2026 -

Fintech & Payments

POS Transactions to Reach $41 Trillion Globally by 2031, as Convergence Towards Unified Commerce Surges

July 2026 -

Fintech & Payments

Digital Travel Credentials: 1.2 Billion Passengers to Adopt DTCs Globally by 2035, Fuelled by Passenger Demand for Seamless Journeys

July 2026 -

Fintech & Payments

Network Tokenisation to Secure 2.4 Trillion Global Transactions Between 2026 and 2030 – Representing 86% of Applicable Transactions

July 2026