Why B2B Payment Cards Are Becoming Essential for Modern Businesses

B2B payments are undergoing a structural shift. According to our latest research, global B2B card payments are set to reach $11 trillion in transaction value; underlining how rapidly cards are moving from a niche tool to a core payment rail for businesses.

This growth is being driven by a simple reality: traditional B2B payment methods are too slow, too opaque, and too manual. As businesses look to digitise procurement, reduce fraud exposure, and gain tighter control over distributed spend, payment cards are stepping in as a more flexible, controllable alternative.

More importantly, cards are no longer just about making payments: they are becoming a way to actively manage them.

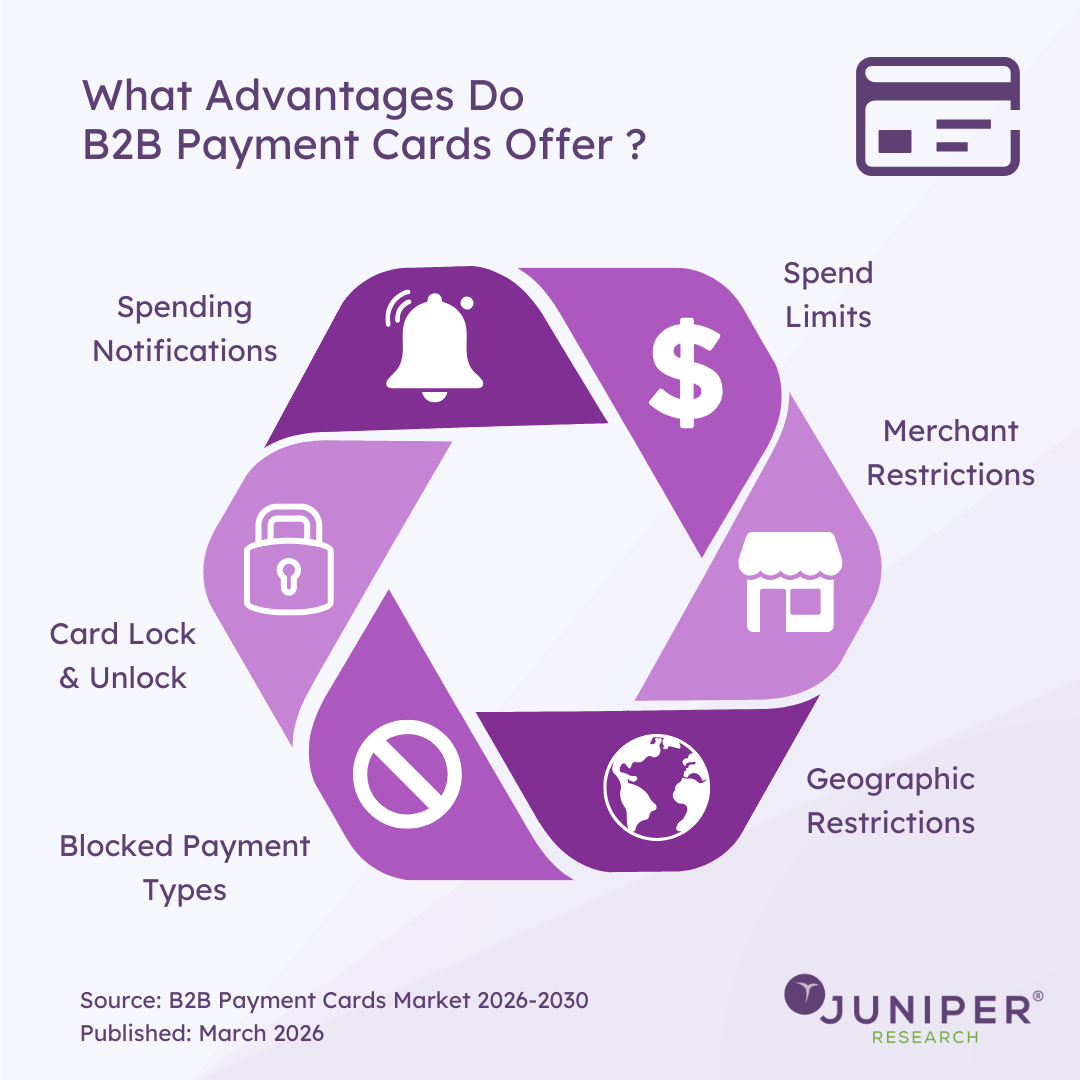

Spending Notifications

Real-time spending notifications give finance teams immediate visibility over transactions as they happen.

This transforms financial oversight. Instead of waiting for reconciliation cycles or monthly reports, businesses can track spend in real time, identify anomalies instantly, and intervene before issues escalate. For organisations managing multiple teams or suppliers, this level of visibility is critical to maintaining control.

Spend Limits

B2B cards enable highly granular control over spending thresholds.

Limits can be set at the level of individuals, departments, or specific use cases, allowing businesses to decentralise purchasing without losing control. This removes friction from procurement processes, while ensuring that spending remains aligned with budgets and policies.

Merchant Restrictions

Merchant-level controls allow businesses to define exactly where funds can be used.

By restricting transactions to approved vendors or merchant categories, organisations can enforce procurement rules automatically. This reduces reliance on manual approvals and post-spend audits, embedding policy enforcement directly into the payment itself.

Geographic Restrictions

Geographic restrictions help businesses align spending with their operational footprint.

Cards can be limited to specific countries or regions, reducing exposure to fraud and preventing unauthorised international transactions. For globally distributed organisations, this provides an essential layer of risk management.

Blocked Payment Types

Businesses can block specific transaction types entirely.

This includes high-risk or unnecessary payment categories such as cash withdrawals or certain online transactions. By removing these options at the source, companies reduce fraud risk and eliminate unwanted spend before it occurs, rather than trying to recover it afterwards.

Card Lock & Unlock

The ability to instantly lock and unlock cards provides real-time security control.

If a card is lost, stolen, or behaving suspiciously, it can be frozen immediately without cancelling the account. This minimises disruption for employees, while giving finance teams confidence that risks can be contained instantly.

Source: B2B Payment Cards Market 2026-2030

Read the Press Release: B2B Card Payments to Reach $11 Trillion Globally in 2030, Accelerated by Increased Corporate Use

Download the Whitepaper: How B2B Payment Cards Are Streamlining Corporate Expenses

Latest research, whitepapers & press releases

-

ReportApril 2026IoT & Emerging Technology

ReportApril 2026IoT & Emerging Technology Molly GatfordPhysical AI in Manufacturing & Logistics Market: 2026-2030

Molly GatfordPhysical AI in Manufacturing & Logistics Market: 2026-2030Our Physical AI in Manufacturing and Logistics research suite provides in-depth analysis of the key economic, operational, and technological factors driving growth in this fast-growing market.

VIEW -

ReportApril 2026Fintech & Payments

ReportApril 2026Fintech & Payments Nick MaynardAgentic Commerce Market: 2026-2031

Nick MaynardAgentic Commerce Market: 2026-2031Juniper Research’s Agentic Commerce research suite provides an insightful analysis of this rapidly emerging market; enabling stakeholders, including AI developers, payment infrastructure providers, eCommerce marketplaces, merchants and many others, to understand future growth, key trends, and the competitive environment.

VIEW -

ReportMarch 2026Fintech & Payments

ReportMarch 2026Fintech & Payments Michael GreenwoodB2B Payment Cards Market: 2026-2030

Michael GreenwoodB2B Payment Cards Market: 2026-2030Our B2B card payments research suite provides detailed analysis of this rapidly changing market; allowing B2B card providers to gain an understanding of key payment trends and challenges, potential growth opportunities, and the competitive environment.

VIEW -

ReportMarch 2026Telecoms & Connectivity

ReportMarch 2026Telecoms & Connectivity Alex WebbDirect Carrier Billing Market: 2026-2030

Alex WebbDirect Carrier Billing Market: 2026-2030Our Direct Carrier Billing research suite for mobile network operators provides detailed analysis and strategic recommendations for the direct carrier billing market over the next four years.

VIEW -

ReportMarch 2026Fintech & Payments

ReportMarch 2026Fintech & Payments Lorien CarterCross-border Payments Market: 2026-2030

Lorien CarterCross-border Payments Market: 2026-2030Our Cross-border Payments research suite provides a comprehensive and in-depth analysis of the evolving cross-border payments landscape; enabling stakeholders such as businesses, financial institutions, payment service providers, card networks, regulators, and technology infrastructure providers to understand future growth, key trends, and the competitive environment.

VIEW -

ReportFebruary 2026Telecoms & Connectivity

ReportFebruary 2026Telecoms & Connectivity Ardit BallhysaMobile Messaging Market: 2026-2030

Ardit BallhysaMobile Messaging Market: 2026-2030Juniper Research’s Mobile Messaging research suite provides mobile messaging vendors, mobile network operators, and enterprises with intelligence on how to capitalise on changing market dynamics within the mobile messaging market.

VIEW

-

WhitepaperApril 2026IoT & Emerging Technology

Molly Gatford

WhitepaperApril 2026IoT & Emerging Technology

Molly GatfordKey Growth Opportunities for Physical AI in 2026

Our complimentary whitepaper, Key Growth Opportunities for Physical AI in 2026, provides insight into the rapidly evolving physical AI in manufacturing and logistics market; highlighting the countries in which high demand for automation in these industries is anticipated over the next five years.

VIEW -

WhitepaperApril 2026Fintech & Payments

Nick Maynard

WhitepaperApril 2026Fintech & Payments

Nick MaynardAgentic Commerce - Revolution or False Dawn?

Our complimentary whitepaper assesses the trends that are increasing agentic commerce adoption, and challenges to agentic commerce usage. Additionally, it includes a forecast summary of the global spend on agentic commerce by 2030.

VIEW -

WhitepaperMarch 2026Fintech & Payments

Michael Greenwood

WhitepaperMarch 2026Fintech & Payments

Michael GreenwoodHow B2B Payment Cards Are Streamlining Corporate Expenses

Our complimentary whitepaper, How B2B Payment Cards Are Streamlining Corporate Expenses, examines the state of the B2B payment cards market; considering its impact on different geographies and how it is shaping the modern B2B payments landscape through card controls, payment data analysis tools, and fully integrated spend management solutions.

VIEW -

WhitepaperMarch 2026Telecoms & Connectivity

Alex Webb

WhitepaperMarch 2026Telecoms & Connectivity

Alex WebbDirect Carrier Billing: Unlocking Emerging Revenue Streams for Operators

Our complimentary whitepaper, Direct Carrier Billing: Unlocking Emerging Revenue Streams for Operators, explores the emerging opportunities for mobile network operators to monetise direct carrier billing.

VIEW -

WhitepaperMarch 2026Telecoms & Connectivity

Molly Gatford

WhitepaperMarch 2026Telecoms & Connectivity

Molly GatfordMWC 2026: What's Next for Mobile?

Our latest whitepaper distils the most important announcements from MWC Barcelona 2026 and examines what they mean for the telecoms market over the year ahead. From network APIs and 5G monetisation to AI-RAN, direct-to-cell connectivity, and 5G-Advanced, it explains where the biggest opportunities — and challenges — will emerge next.

VIEW -

WhitepaperMarch 2026Fintech & Payments

Lorien Carter

WhitepaperMarch 2026Fintech & Payments

Lorien CarterThe Transformation of Cross-border Payment Infrastructure

Our complimentary whitepaper, The Transformation of Cross-border Payment Infrastructure, examines the state of the cross-border payments market; explaining the role of key actors in transforming the cross-border payment experience, as well as the current landscape and recent developments within the cross-border payments industry.

VIEW

-

IoT & Emerging Technology

Physical AI Deployments in Manufacturing & Logistics to Reach 400,000 Systems by 2030

April 2026 -

Fintech & Payments

Agentic Commerce Set to Generate $1.5 Trillion Globally by 2030, as Payments Infrastructure Leaders Revealed

April 2026 -

Fintech & Payments

B2B Card Payments to Reach $11 Trillion Globally in 2030, Accelerated by Increased Corporate Use

March 2026 -

Telecoms & Connectivity

Direct Carrier Billing to Grow by $35 Billion Globally Over the Next Four Years, as Anti-fraud Capabilities Are Enhanced by Network APIs

March 2026 -

Fintech & Payments

Sophisticated Microfinance Services Spend to Surpass $22 billion By 2030, as Mobile Money Services in Emerging Markets Mature

March 2026 -

Fintech & Payments

Top Three Global Leaders in Cross-border Payment Infrastructure Revealed

March 2026