The Iran Ceasefire Might Stabilise the Middle East — But Can the AI Boom Recover?

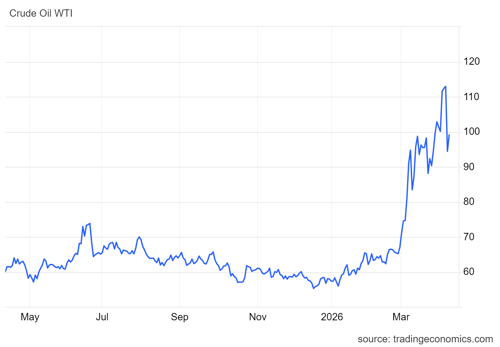

Tanker traffic through the Strait of Hormuz has effectively ground to a halt, down from an average of 138 vessels per day in peacetime. The impact on oil markets has been immediate and severe; marking the most significant price shock since the 1970s, with further volatility likely as the conflict evolves. Prior to US strikes on Iran on 26 February, oil was trading at $74 per barrel; it has since surged, hitting peaks of $113.

Crude Oil, $ per Barrel (as of 9th April)

This week’s ceasefire has provided only limited relief. Although prices briefly dipped following the announcement, the truce remains fragile, and shipping through the Strait is still heavily restricted; meaning supply constraints, and elevated prices, are likely to persist in the near term.

This disruption is not confined to oil markets. It feeds directly into the cost and availability of energy inputs that underpin AI infrastructure; particularly natural gas, which remains the primary power source for data centres.

Around 75% of AI data centres run on natural gas as their primary fuel source, as outlined last month by Cleanview. This is because of unavoidable baseline energy demands: local grids cannot provide AI data centres with enough power, and even if they could, connecting to them can take up to five years.

Additionally, solar power and other renewable sources experience fluctuating energy production, while small nuclear reactors are up to a decade away from being realised in a commercial space. The only method deployable today that is capable of generating enough power for AI is natural gas; making it the foundation of the entire AI sector. As a result, any increase in oil prices or limiting of supply represents a material threat to the AI industry — a risk already highlighted by Iran’s attack on Qatar’s Ras Laffan Industrial City, the world’s largest liquefied natural gas facility.

Electricity accounts for around half the expenses of an AI data centre. With the sharp surges in energy prices affecting bottom-line expenses, it will become even harder for AI startups to become profitable. Downstream effects such as increased subscription prices or usage caps might reduce demand for AI subscriptions, as well as causing investors to think twice before supporting the AI industry.

Helium Shortages

At the start of the year, we wrote about the deleterious effects of AI on consumer chip prices. In short, AI hyperscalers were outbidding consumer manufacturers for access to chips; causing prices to soar and smaller AI startups to be locked out of RAM access - now, AI and computer chips are in the headlines again.

Helium is critical to the process of building advanced microchips for AI. A third of all commercial helium is produced in just three helium plants, located in Qatar. The immediate effect of the closing of the Strait of Hormuz is that helium tanks are stuck in Qatar, unable to transit. At the moment, the impact of this on supply is mitigated by the recent 15% surplus of helium compared to global demand. However, if the war continues then these supplies will deplete. Furthermore, as helium is produced from waste products of liquified natural gas (LNG) plants, when these plants have to cease production - when their LNG storage tanks are filled - it will have a knock-on effect on helium production. At worst, this could close a third of helium production; devastating semiconductor manufacturers and, once again, increasing prices.

Threats on AI Data Centres

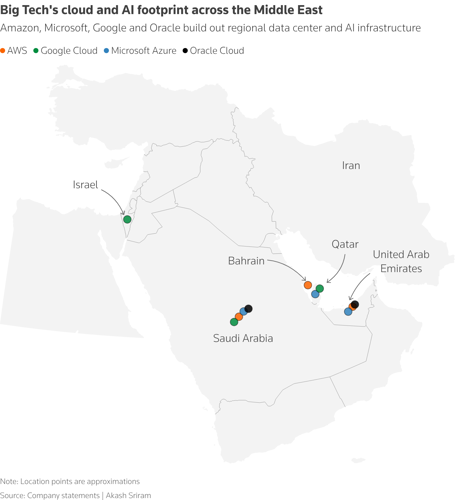

For the first time ever, commercial data centres have become targets for warfare. Several data centres in the Middle East region have been struck by missiles: Amazon Web Services has had data centres struck in Bahrain and Oracle has had one hit in Dubai. These strikes had the effect of wiping out access to mobile banking services and fintech-based payments for millions in the region.

What’s more, Iran has stated that if the US hits civilian infrastructure such as power plants and water desalination plants, they will retaliate with strikes against the energy and technology infrastructure of US companies - specifically, the Stargate data centre in the UAE, which is jointly owned by OpenAI, SoftBank, and Oracle. This unprecedented move recognises AI infrastructure as a sovereign asset.

Regardless of how quickly this current war ends, the positioning of data centres as valuable targets will not be forgotten. It costs billions to build one single data centre capable of meeting the requirements needed to power AI, and only seconds to completely wipe it out. This reliance on exposed core infrastructure may cause investors to pull back.

What of the Future?

No matter how quickly the war ends, ongoing shocks to supply will continue. Existing attacks on oil production plants have eliminated production capacity for years to come. For example, attacks on the LNG plant in Ras Laffan has been estimated to wipe out 3.5% of global LNG production for the next three to five years. This will increase energy costs in the long term; impacting AI’s supply chain and operating costs.

One potential long-term effect stems from the geographical divergence in AI growth, which could result in regions such as North America and South Asia racing forward with AI while Europe and the Middle East are held back. Europe is more exposed to oil price shocks than the US - seeing prices rise 40% compared to only 5% in the US - so oil price rises will hit Europe-based AI companies harder. Similarly, the conflict risk to infrastructure may cause Chinese companies such as Alibaba and Huawei to redirect data centre investment away from the Middle East; interrupting the Gulf’s ambition to become an AI frontrunner.

While the US is initially more insulated from oil price rises, the long-term economic impacts of the war may yet put its entire AI industry at risk.

Related Research

-

ReportApril 2026IoT & Emerging Technology

ReportApril 2026IoT & Emerging Technology Molly GatfordPhysical AI in Manufacturing & Logistics Market, 2026-2030

Molly GatfordPhysical AI in Manufacturing & Logistics Market, 2026-2030Our Physical AI in Manufacturing and Logistics research suite provides in-depth analysis of the key economic, operational, and technological factors driving growth in this fast-growing market.

VIEW -

ReportApril 2026Fintech & Payments

ReportApril 2026Fintech & Payments Nick MaynardAgentic Commerce Market, 2026-2031

Nick MaynardAgentic Commerce Market, 2026-2031Juniper Research’s Agentic Commerce research suite provides an insightful analysis of this rapidly emerging market; enabling stakeholders, including AI developers, payment infrastructure providers, eCommerce marketplaces, merchants and many others, to understand future growth, key trends, and the competitive environment.

VIEW -

ReportDecember 2025Telecoms & Connectivity

Molly GatfordAI Agents for Customer Experience Platforms Market, 2025-2030

ReportDecember 2025Telecoms & Connectivity

Molly GatfordAI Agents for Customer Experience Platforms Market, 2025-2030Our comprehensive AI Agents for Customer Experience Platforms research suite comprises detailed assessment of a market that is set to disrupt mobile communications. It provides stakeholders with insight into the key opportunities within the AI agents for customer experience platforms market over the next two years.

VIEW

Latest research, whitepapers & press releases

-

ReportApril 2026IoT & Emerging Technology

ReportApril 2026IoT & Emerging Technology Molly GatfordPhysical AI in Manufacturing & Logistics Market: 2026-2030

Molly GatfordPhysical AI in Manufacturing & Logistics Market: 2026-2030Our Physical AI in Manufacturing and Logistics research suite provides in-depth analysis of the key economic, operational, and technological factors driving growth in this fast-growing market.

VIEW -

ReportApril 2026Fintech & Payments

ReportApril 2026Fintech & Payments Nick MaynardAgentic Commerce Market: 2026-2031

Nick MaynardAgentic Commerce Market: 2026-2031Juniper Research’s Agentic Commerce research suite provides an insightful analysis of this rapidly emerging market; enabling stakeholders, including AI developers, payment infrastructure providers, eCommerce marketplaces, merchants and many others, to understand future growth, key trends, and the competitive environment.

VIEW -

ReportMarch 2026Fintech & Payments

ReportMarch 2026Fintech & Payments Michael GreenwoodB2B Payment Cards Market: 2026-2030

Michael GreenwoodB2B Payment Cards Market: 2026-2030Our B2B card payments research suite provides detailed analysis of this rapidly changing market; allowing B2B card providers to gain an understanding of key payment trends and challenges, potential growth opportunities, and the competitive environment.

VIEW -

ReportMarch 2026Telecoms & Connectivity

ReportMarch 2026Telecoms & Connectivity Alex WebbDirect Carrier Billing Market: 2026-2030

Alex WebbDirect Carrier Billing Market: 2026-2030Our Direct Carrier Billing research suite for mobile network operators provides detailed analysis and strategic recommendations for the direct carrier billing market over the next four years.

VIEW -

ReportMarch 2026Fintech & Payments

ReportMarch 2026Fintech & Payments Lorien CarterCross-border Payments Market: 2026-2030

Lorien CarterCross-border Payments Market: 2026-2030Our Cross-border Payments research suite provides a comprehensive and in-depth analysis of the evolving cross-border payments landscape; enabling stakeholders such as businesses, financial institutions, payment service providers, card networks, regulators, and technology infrastructure providers to understand future growth, key trends, and the competitive environment.

VIEW -

ReportFebruary 2026Telecoms & Connectivity

ReportFebruary 2026Telecoms & Connectivity Ardit BallhysaMobile Messaging Market: 2026-2030

Ardit BallhysaMobile Messaging Market: 2026-2030Juniper Research’s Mobile Messaging research suite provides mobile messaging vendors, mobile network operators, and enterprises with intelligence on how to capitalise on changing market dynamics within the mobile messaging market.

VIEW

-

WhitepaperApril 2026IoT & Emerging Technology

Molly Gatford

WhitepaperApril 2026IoT & Emerging Technology

Molly GatfordKey Growth Opportunities for Physical AI in 2026

Our complimentary whitepaper, Key Growth Opportunities for Physical AI in 2026, provides insight into the rapidly evolving physical AI in manufacturing and logistics market; highlighting the countries in which high demand for automation in these industries is anticipated over the next five years.

VIEW -

WhitepaperApril 2026Fintech & Payments

Nick Maynard

WhitepaperApril 2026Fintech & Payments

Nick MaynardAgentic Commerce - Revolution or False Dawn?

Our complimentary whitepaper assesses the trends that are increasing agentic commerce adoption, and challenges to agentic commerce usage. Additionally, it includes a forecast summary of the global spend on agentic commerce by 2030.

VIEW -

WhitepaperMarch 2026Fintech & Payments

Michael Greenwood

WhitepaperMarch 2026Fintech & Payments

Michael GreenwoodHow B2B Payment Cards Are Streamlining Corporate Expenses

Our complimentary whitepaper, How B2B Payment Cards Are Streamlining Corporate Expenses, examines the state of the B2B payment cards market; considering its impact on different geographies and how it is shaping the modern B2B payments landscape through card controls, payment data analysis tools, and fully integrated spend management solutions.

VIEW -

WhitepaperMarch 2026Telecoms & Connectivity

Alex Webb

WhitepaperMarch 2026Telecoms & Connectivity

Alex WebbDirect Carrier Billing: Unlocking Emerging Revenue Streams for Operators

Our complimentary whitepaper, Direct Carrier Billing: Unlocking Emerging Revenue Streams for Operators, explores the emerging opportunities for mobile network operators to monetise direct carrier billing.

VIEW -

WhitepaperMarch 2026Telecoms & Connectivity

Molly Gatford

WhitepaperMarch 2026Telecoms & Connectivity

Molly GatfordMWC 2026: What's Next for Mobile?

Our latest whitepaper distils the most important announcements from MWC Barcelona 2026 and examines what they mean for the telecoms market over the year ahead. From network APIs and 5G monetisation to AI-RAN, direct-to-cell connectivity, and 5G-Advanced, it explains where the biggest opportunities — and challenges — will emerge next.

VIEW -

WhitepaperMarch 2026Fintech & Payments

Lorien Carter

WhitepaperMarch 2026Fintech & Payments

Lorien CarterThe Transformation of Cross-border Payment Infrastructure

Our complimentary whitepaper, The Transformation of Cross-border Payment Infrastructure, examines the state of the cross-border payments market; explaining the role of key actors in transforming the cross-border payment experience, as well as the current landscape and recent developments within the cross-border payments industry.

VIEW

-

IoT & Emerging Technology

Physical AI Deployments in Manufacturing & Logistics to Reach 400,000 Systems by 2030

April 2026 -

Fintech & Payments

Agentic Commerce Set to Generate $1.5 Trillion Globally by 2030, as Payments Infrastructure Leaders Revealed

April 2026 -

Fintech & Payments

B2B Card Payments to Reach $11 Trillion Globally in 2030, Accelerated by Increased Corporate Use

March 2026 -

Telecoms & Connectivity

Direct Carrier Billing to Grow by $35 Billion Globally Over the Next Four Years, as Anti-fraud Capabilities Are Enhanced by Network APIs

March 2026 -

Fintech & Payments

Sophisticated Microfinance Services Spend to Surpass $22 billion By 2030, as Mobile Money Services in Emerging Markets Mature

March 2026 -

Fintech & Payments

Top Three Global Leaders in Cross-border Payment Infrastructure Revealed

March 2026