Pay by Bank Pursues the American Dream

Last month, US-based cloud payment orchestration platform Gr4vy announced its partnership with Open Banking data network Plaid to enable merchants using Gr4vy to offer Pay by Bank at checkout.

This partnership will allow Pay by Bank, also called account-to-account (A2A) payments, to be offered through a single integration by giving access to Plaid’s bank connectivity; allowing customers to authenticate and pay directly from their bank account at checkout. Plaid’s network is connected to over 12,000 financial institutions across the US, Canada, the UK, and Europe.

Source: Gr4vy

What makes this partnership particularly noteworthy is Plaid’s strong presence in the US - a market where Pay by Bank is not well established. The payment method is far more mature in the UK and EU due to the strength of Open Banking regulation. In 2018, the EU required all banks to share their customers’ data securely with authorised third-party providers via APIs, with the introduction of the Revised Payment Service Directive (PSD2). This regulation allows Pay by Bank providers to offer the service for consumers without the need for individual agreements with each bank; making it far easier to achieve widespread coverage. This has seen a surge in Pay by Bank in these markets, with 10 million people using Pay by Bank monthly in the UK.

This contrasts with the US, where there are not strong and clear Open Banking regulations. In October 2023, the Consumer Financial Protection Bureau (CFPB) proposed a rule to implement section 1033 of the Consumer Financial Protection Act, which would give consumers the right to access and share their financial data.

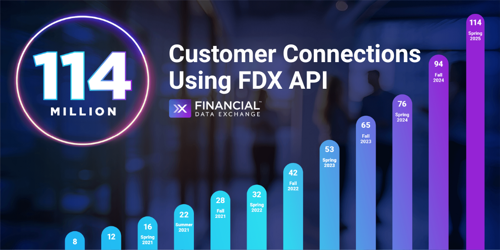

This rule, if adopted, would establish a clear federal regulation for Open Banking, with the CFPB overseeing its implementation. As things stand, these rules have not been implemented and the CFPB is facing restructuring; casting doubts over the potential implementation of this regulation. Alongside this, several states have implemented, or are considering implementing, their own Open Banking legislation. There are also industry-led initiatives, such as the Financial Data Exchange (FDX), that are establishing voluntary data-sharing standards. The FDX is a non-profit industry standards body that created the FDX API - a technical standard for sharing financial data. The FDX has 200 member organisations connecting 114 million customer accounts.

Source: FDX

This demonstrates the fragmented nature of the Open Banking space within the US. This presents challenges for Pay by Bank providers looking to grow the payment method within the US, as it means the quality of coverage varies extensively by region; limiting its appeal to major brands. In particular, Pay by Bank providers in the UK have been successful in gaining buy-in from large eCommerce marketplaces, such as Amazon and eBay, which plays an important role in normalising the payment method for eCommerce. In a market such as the US, where access to consumers’ accounts is patchy, there is less reason for a national player such as Amazon to offer Pay by Bank, as a significant proportion of its customer base will not be able to use it.

The key selling point of Pay by Bank to merchants is lower fees compared to credit and debit cards. However, this is not the only advantage to merchants: a Pay by Bank transaction is authenticated by the user’s bank when they initiate the transaction; reducing the burden of verifying the consumer on the merchant.

Another benefit for merchants is the lack of a chargeback process. Chargebacks are a significant cost for merchants, with friendly fraud being a significant concern for eCommerce merchants in particular. As there is no chargeback mechanism and transactions are finalised immediately, a merchant does not need to worry about revenue being taken and incurring costly fees on top of that. This does not remove a merchant’s requirement to offer refunds, but does speed up the process for the consumer. These are all strong motives for merchants to adopt; however, in the US, merchants are put off by the fragmented nature of consumer availability.

The fundamental issue for Pay by Bank in the US is one of connecting merchants to the customers. Without the federal government implementing nationwide Open Banking requirements, Juniper Research believes that Pay by Bank will be limited to a more niche payment option.

However, if regulations enable Open Banking to offer far wider coverage, then Pay by Bank offers solutions to significant pain points for merchants. In particular, high card fees in the US make Pay by Bank even more appealing than in markets where it has already taken off. Juniper Research recommends that Pay by Bank providers continue to work closely with Open Banking networks to broaden the number of customers able to use Pay by Bank, while proactively working with regulators to support Open Banking regulations.

As a Senior Research Analyst, Michael delivers in-depth insights into the fast-evolving worlds of digital identity and payments. His recent work spans critical topics such as B2B Payment Cards, B2B Payments, and Chargeback Management; helping industry leaders navigate change and identify new opportunities.

Related Research

-

ReportSeptember 2025Fintech & Payments

ReportSeptember 2025Fintech & Payments Thomas WilsonA2A Payments Market, 2025-2030

Thomas WilsonA2A Payments Market, 2025-2030Our A2A Payments research suite provides detailed analysis of this rapidly changing market; enabling A2A payments service providers to gain an understanding of key payment trends and challenges, potential growth opportunities, and the competitive environment.

VIEW -

ReportJune 2026Fintech & Payments

ReportJune 2026Fintech & Payments Michael GreenwoodChargeback Management Market, 2026-2031

Michael GreenwoodChargeback Management Market, 2026-2031Our Chargeback Management research suite provides detailed analysis of this fast-changing market; allowing chargeback management providers to gain an understanding of key payment trends and challenges, potential growth opportunities, and the competitive environment.

VIEW -

ReportDecember 2025Fintech & Payments

ReportDecember 2025Fintech & Payments Shane O'SullivaneCommerce Fraud Prevention Market, 2025-2030

Shane O'SullivaneCommerce Fraud Prevention Market, 2025-2030Our eCommerce Fraud Prevention research suite provides a detailed and insightful analysis of this evolving market; enabling stakeholders from financial institutions, law enforcement agencies, regulatory bodies and technology vendors to understand future growth, key trends, and the competitive environment.

VIEW

Latest research, whitepapers & press releases

-

ReportJuly 2026IoT & Emerging Technology

ReportJuly 2026IoT & Emerging Technology Saffron DusanjhVLEO Satellite Market: 2026-2031

Saffron DusanjhVLEO Satellite Market: 2026-2031Our Very Low Earth Orbit (VLEO) Satellite Market research suite provides comprehensive analysis of one of the fastest-emerging markets within the global space economy.

VIEW -

ReportJuly 2026Telecoms & Connectivity

ReportJuly 2026Telecoms & Connectivity Alex WebbIPX Providers Competitor Leaderboard: 2026

Alex WebbIPX Providers Competitor Leaderboard: 2026Our IPX Providers Competitor Leaderboard 2026 delivers comprehensive evaluation and examination of 16 leading IPX vendors. It provides mobile network operators and other IPX customers with profiles, competitor benchmarking, and strategic analysis of these leading providers.

VIEW -

ReportJuly 2026Fintech & Payments

ReportJuly 2026Fintech & Payments Jawad JahanPOS Market: 2026-2031

Jawad JahanPOS Market: 2026-2031Our Point of Sale (POS) Market research suite provides detailed and insightful analysis of this evolving market; enabling stakeholders - from POS hardware manufacturers, payment infrastructure providers, software developers, and hospitality and retail vendors - to understand future growth, key trends, and the competitive environment.

VIEW -

ReportJuly 2026Fintech & Payments

ReportJuly 2026Fintech & Payments Shane O'SullivanDigital Travel Credential Market: 2026-2035

Shane O'SullivanDigital Travel Credential Market: 2026-2035Our Digital Travel Credential Market research suite provides detailed analysis of this rapidly changing market; allowing digital travel credential solution providers, regulatory bodies, border control authorities, airlines, and airport operators to gain a comprehensive understanding of key digital travel trends, implementation challenges, future growth opportunities, and the competitive environment.

VIEW -

ReportJuly 2026Fintech & Payments

ReportJuly 2026Fintech & Payments Thomas WilsonNetwork Tokenisation Market: 2026-2031

Thomas WilsonNetwork Tokenisation Market: 2026-2031Our Network Tokenisation research suite provides a comprehensive and in-depth analysis of the ecosystem surrounding network tokenisation, enabling stakeholders such as merchants, payment gateways, token service providers and token requestors to understand future growth, key trends and the competitive environment.

VIEW -

ReportJuly 2026Telecoms & Connectivity

Alex WebbSponsored Roaming Competitor Leaderboard: 2026

ReportJuly 2026Telecoms & Connectivity

Alex WebbSponsored Roaming Competitor Leaderboard: 2026Our Sponsored Roaming Competitor Leaderboard 2026 delivers competitor benchmarking and analysis of 14 leading sponsored roaming vendors.

VIEW

-

WhitepaperJuly 2026Fintech & Payments

Jawad Jahan

WhitepaperJuly 2026Fintech & Payments

Jawad JahanFrom Transaction to Transformation: The Future of POS

Our complimentary whitepaper, From Transaction to Transformation: The Future of POS, analyses the current landscape of the POS market. It also provides insight into key trends shaping the POS market, such as POS terminals increasingly being used as a business management platform.

VIEW -

WhitepaperJuly 2026Fintech & Payments

Shane O'Sullivan

WhitepaperJuly 2026Fintech & Payments

Shane O'SullivanBeyond the Boarding Pass: The Digital Travel Credential Paradigm

Our complimentary whitepaper, Beyond the Boarding Pass: The Digital Travel Credential Paradigm, examines the rapidly evolving state of the digital travel credential market.

VIEW -

WhitepaperJuly 2026Fintech & Payments

Thomas Wilson

WhitepaperJuly 2026Fintech & Payments

Thomas WilsonThe Top Three Drivers of Network Tokenisation Adoption

Our complimentary whitepaper, The Top Three Drivers of Network Tokenisation Adoption, examines the state of the network tokenisation market; considering its impact on different payment modalities, how it is shaping the modern payments landscape through safer, more secure payments, and how it could unlock the potential of agentic commerce.

VIEW -

WhitepaperJune 2026Fintech & Payments

WhitepaperJune 2026Fintech & Payments Nick Maynard

Nick MaynardMoney20/20 Europe 2026 Key Takeaways: What You Need to Know Post-event

Money 20/20 Europe once again brought together people from across the fintech, payments and identity ecosystems; creating three days of discussions, announcements and networking.

VIEW -

WhitepaperJune 2026Fintech & Payments

WhitepaperJune 2026Fintech & Payments Michael Greenwood

Michael GreenwoodChargeback Management: The Fightback Against Friendly Fraud

Our complimentary whitepaper, Chargeback Management: The Fightback Against Friendly Fraud, examines the growing impact of friendly fraud on the chargeback management space, as well as how chargeback management tools are mitigating this threat.

VIEW -

WhitepaperJune 2026Telecoms & Connectivity

WhitepaperJune 2026Telecoms & Connectivity Peter Boyland

Peter BoylandAgentic and Conversational AI: Streamlining Revenue Opportunities

Our complimentary whitepaper, Agentic and Conversational AI: Streamlining Revenue Opportunities, explores the challenges and opportunities for operators and enterprises as conversational AI becomes more embedded in the consumer experience.

VIEW

-

Telecoms & Connectivity

Juniper Research Identifies Syniverse, BICS, and iBASIS as Leaders in the IPX Market

July 2026 -

Fintech & Payments

POS Transactions to Reach $41 Trillion Globally by 2031, as Convergence Towards Unified Commerce Surges

July 2026 -

Fintech & Payments

Digital Travel Credentials: 1.2 Billion Passengers to Adopt DTCs Globally by 2035, Fuelled by Passenger Demand for Seamless Journeys

July 2026 -

Fintech & Payments

Network Tokenisation to Secure 2.4 Trillion Global Transactions Between 2026 and 2030 – Representing 86% of Applicable Transactions

July 2026 -

Telecoms & Connectivity

Juniper Research Identifies BICS, Telna, and Vodafone Procure & Connect as Leaders in the Sponsored Roaming Market

July 2026 -

Fintech & Payments

Digital Identity Verification Checks to Reach 175 Billion Globally by 2030, with Biometric Verification the Fastest-growing Modality

July 2026