Building a Successful Superapp: Lessons from Careem

Superapps have been a major point of discussion in the fintech space for several years, with many payment apps and digital wallets having ambitions to become one. The primary motivation for becoming a superapp is the expansion of revenue streams, which can increase an app’s profitability and diversify its sources of revenue, protecting the business from a downturn in any one area.

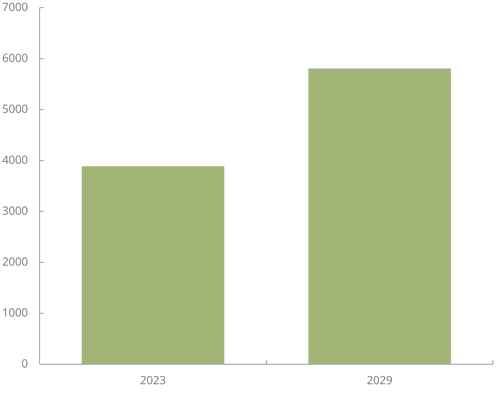

Given this advantage, it is easy to understand why a digital wallet would want to become a fully fledged super app. There is clearly growing potential for this, with our latest forecasts showing that the number of people using digital wallets will grow by 46% between 2024 and 2029.

Number of People Using Digital Wallets (m), 2024 and 2029

Source: Juniper Research

For businesses looking to adopt the superapp model, it is important to understand how other successful superapps have gained their position in their respective markets.

Let's look at Careem.

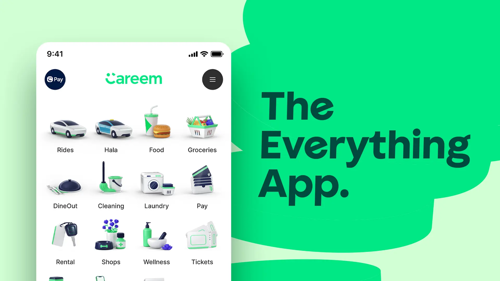

Careem was founded in 2012 in the UAE as a ride-hailing app. Since its launch, it has expanded its geographic coverage, and is now available in cities in Qatar, Saudi Arabia, Egypt, Morocco, Pakistan, Jordan, Iraq, Bahrain, and Kuwait. It has also expanded into groceries, deliveries, and payments. By 2024, Careem had more than 48 million customers across 80 cities in the 10 countries in which it operates.

Almost all superapps start off as specialised apps; in Careem’s case this was as a ride-hailing app. The advantage of starting off in this way is that it requires less development to get a working app ready to deploy compared with a more broadly focused one; allowing for lower costs and faster time to market. Another strength of this method is that it allows the app to target a specific gap in the market to build up a user base.

Source: Careem

It is important that, if a brand is launching a specialised app, with the intention of it becoming a superapp, the app is designed with modularity in mind. This will make it easier to integrate new features into the app as it grows. One effective way to go about this would be to build the app using a third-party platform. This is cheaper than hiring a development team to build it, and it allows the new app to benefit from the experience of the platform provider. It is crucial that a business selects the right platform for their app as, once one is selected, the vendor is limited by the platform’s capabilities. This means that selecting the wrong platform can prevent a vendor from expanding its capabilities into new areas as opportunities present themselves.

Once an app is established, the next step is to grow it. This is in terms of user base, geographic coverage, and range of services offered. In Careem’s case, it took the approach of focusing on expanding geographically. Between 2012 and 2017, it expanded to cover the 10 countries it covers today, but the only added features were ones which strengthened its ride-sharing business. This strategy grows the user base, building trust and familiarity with users. Due to this, as services expand, existing customers are more likely to adopt a new service from a provider with which they are already familiar.

A payment feature is a consistent part of most superapps. This allows the app to facilitate payments for its own services internally, as well as to tap into revenue from different types of money transfers. Careem first entered into the digital payment space with Careem Pay, a closed-loop P2P money transfer system. This was expanded into a full open-loop payment wallet in 2020, which allowed it to make payments and withdraw funds from the ecosystem. In 2023, Careem added remittances, starting off with the UAE-Pakistan corridor. This was to take advantage of the fact many of its drivers were Pakistani citizens who already transferred their income back to Pakistan. This was sufficiently successful that it has since expanded to include remittance corridors to the UK, India, and the Philippines.

This shows two important trends to making a successful superapp: understanding users and integrating suitable new services with existing ones. Careem understood that many its users were migrant workers who would be sending money to their home country. As these workers were earning money as drivers on the Careem app, this meant it already stored the money the user wished to transfer. This combined the ride-hailing element of the app with the remittance feature; creating an overall stronger offering. When adding new features, particularly payment ones, a brand must look at who its customer base is and what services it already offers. By offering services that synergise with existing offerings, and targeting existing customers, an app can maximise the chances of a new feature’s success. The downside to this is it focuses on an existing user base; potentially limiting its ability to grow the total customer base.

Source: infinum

Careem sets a clear example of how to grow a specialised app into a superapp, with others such as Grab and Gojek following similar paths. Vendors looking to launch an app or expand an existing one must understand what these success stories did to get to where they are, and draw relevant lessons for themselves. Key considerations are modularity from the beginning to simplify the process of expanding the wallet as it grows, targeting features to a specific audience or a gap in the market, and using inbuilt payments and funds to provide a seamless checkout experience and keep a user’s money within the superapp ecosystem.

Michael is a Senior Research Analyst at Juniper Research, and primarily conducts research on digital identity and payments markets. His recent reports include Digital Wallets, Digital Identity, and Instant Payments.

Related Research

-

ReportNovember 2025Digital Wallets

ReportNovember 2025Digital Wallets Thomas WilsonDigital Wallets Market, 2025-2030

Thomas WilsonDigital Wallets Market, 2025-2030Our digital wallets research suite provides detailed analysis of this rapidly changing market; allowing digital wallet providers to gain an understanding of key payment trends and challenges, potential growth opportunities, and the competitive environment.

VIEW

Latest research, whitepapers & press releases

-

ReportJuly 2026IoT & Emerging Technology

ReportJuly 2026IoT & Emerging Technology Saffron DusanjhVLEO Satellite Market: 2026-2031

Saffron DusanjhVLEO Satellite Market: 2026-2031Our Very Low Earth Orbit (VLEO) Satellite Market research suite provides comprehensive analysis of one of the fastest-emerging markets within the global space economy.

VIEW -

ReportJuly 2026Telecoms & Connectivity

ReportJuly 2026Telecoms & Connectivity Alex WebbIPX Providers Competitor Leaderboard: 2026

Alex WebbIPX Providers Competitor Leaderboard: 2026Our IPX Providers Competitor Leaderboard 2026 delivers comprehensive evaluation and examination of 16 leading IPX vendors. It provides mobile network operators and other IPX customers with profiles, competitor benchmarking, and strategic analysis of these leading providers.

VIEW -

ReportJuly 2026Fintech & Payments

ReportJuly 2026Fintech & Payments Jawad JahanPOS Market: 2026-2031

Jawad JahanPOS Market: 2026-2031Our Point of Sale (POS) Market research suite provides detailed and insightful analysis of this evolving market; enabling stakeholders - from POS hardware manufacturers, payment infrastructure providers, software developers, and hospitality and retail vendors - to understand future growth, key trends, and the competitive environment.

VIEW -

ReportJuly 2026Fintech & Payments

ReportJuly 2026Fintech & Payments Shane O'SullivanDigital Travel Credential Market: 2026-2035

Shane O'SullivanDigital Travel Credential Market: 2026-2035Our Digital Travel Credential Market research suite provides detailed analysis of this rapidly changing market; allowing digital travel credential solution providers, regulatory bodies, border control authorities, airlines, and airport operators to gain a comprehensive understanding of key digital travel trends, implementation challenges, future growth opportunities, and the competitive environment.

VIEW -

ReportJuly 2026Fintech & Payments

ReportJuly 2026Fintech & Payments Thomas WilsonNetwork Tokenisation Market: 2026-2031

Thomas WilsonNetwork Tokenisation Market: 2026-2031Our Network Tokenisation research suite provides a comprehensive and in-depth analysis of the ecosystem surrounding network tokenisation, enabling stakeholders such as merchants, payment gateways, token service providers and token requestors to understand future growth, key trends and the competitive environment.

VIEW -

ReportJuly 2026Telecoms & Connectivity

Alex WebbSponsored Roaming Competitor Leaderboard: 2026

ReportJuly 2026Telecoms & Connectivity

Alex WebbSponsored Roaming Competitor Leaderboard: 2026Our Sponsored Roaming Competitor Leaderboard 2026 delivers competitor benchmarking and analysis of 14 leading sponsored roaming vendors.

VIEW

-

WhitepaperJuly 2026IoT & Emerging Technology

Saffron Dusanjh

WhitepaperJuly 2026IoT & Emerging Technology

Saffron DusanjhBeyond LEO: Why VLEO is Becoming the Next Growth Market

Our complimentary whitepaper, Beyond LEO: Why VLEO is Becoming the Next Growth Market, explores how VLEO is transitioning from an experimental orbital regime into a commercially viable market.

VIEW -

WhitepaperJuly 2026Fintech & Payments

Jawad Jahan

WhitepaperJuly 2026Fintech & Payments

Jawad JahanFrom Transaction to Transformation: The Future of POS

Our complimentary whitepaper, From Transaction to Transformation: The Future of POS, analyses the current landscape of the POS market. It also provides insight into key trends shaping the POS market, such as POS terminals increasingly being used as a business management platform.

VIEW -

WhitepaperJuly 2026Fintech & Payments

Shane O'Sullivan

WhitepaperJuly 2026Fintech & Payments

Shane O'SullivanBeyond the Boarding Pass: The Digital Travel Credential Paradigm

Our complimentary whitepaper, Beyond the Boarding Pass: The Digital Travel Credential Paradigm, examines the rapidly evolving state of the digital travel credential market.

VIEW -

WhitepaperJuly 2026Fintech & Payments

Thomas Wilson

WhitepaperJuly 2026Fintech & Payments

Thomas WilsonThe Top Three Drivers of Network Tokenisation Adoption

Our complimentary whitepaper, The Top Three Drivers of Network Tokenisation Adoption, examines the state of the network tokenisation market; considering its impact on different payment modalities, how it is shaping the modern payments landscape through safer, more secure payments, and how it could unlock the potential of agentic commerce.

VIEW -

WhitepaperJune 2026Fintech & Payments

WhitepaperJune 2026Fintech & Payments Nick Maynard

Nick MaynardMoney20/20 Europe 2026 Key Takeaways: What You Need to Know Post-event

Money 20/20 Europe once again brought together people from across the fintech, payments and identity ecosystems; creating three days of discussions, announcements and networking.

VIEW -

WhitepaperJune 2026Fintech & Payments

WhitepaperJune 2026Fintech & Payments Michael Greenwood

Michael GreenwoodChargeback Management: The Fightback Against Friendly Fraud

Our complimentary whitepaper, Chargeback Management: The Fightback Against Friendly Fraud, examines the growing impact of friendly fraud on the chargeback management space, as well as how chargeback management tools are mitigating this threat.

VIEW

-

IoT & Emerging Technology

VLEO Satellites: Global Investment to Near $10 Billion by 2031; Driven by Falling Launch Costs

July 2026 -

Telecoms & Connectivity

Juniper Research Identifies Syniverse, BICS, and iBASIS as Leaders in the IPX Market

July 2026 -

Fintech & Payments

POS Transactions to Reach $41 Trillion Globally by 2031, as Convergence Towards Unified Commerce Surges

July 2026 -

Fintech & Payments

Digital Travel Credentials: 1.2 Billion Passengers to Adopt DTCs Globally by 2035, Fuelled by Passenger Demand for Seamless Journeys

July 2026 -

Fintech & Payments

Network Tokenisation to Secure 2.4 Trillion Global Transactions Between 2026 and 2030 – Representing 86% of Applicable Transactions

July 2026 -

Telecoms & Connectivity

Juniper Research Identifies BICS, Telna, and Vodafone Procure & Connect as Leaders in the Sponsored Roaming Market

July 2026