What Amazon’s Pay by Bank Launch Means for UK eCommerce

Last week, Amazon expanded UK payment options with Pay by Bank through a partnership with TrueLayer.

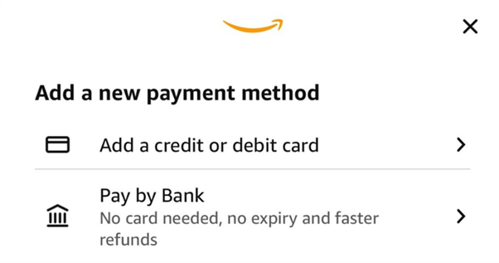

It introduces a card-free, account-to-account (A2A) payment option that lets customers pay directly from their bank accounts using open banking infrastructure. Instead of entering or storing card details, shoppers select their bank at checkout, are securely redirected to their mobile or online banking, and authorise the payment via PIN or biometrics, with funds moving straight from their account to Amazon.

This method mirrors familiar mobile-banking journeys while removing card expiry issues and the need to update stored card details, and it supports near-instant refunds back into the customer’s bank account once returns are processed. Amazon also extends its A-to-Z Guarantee and the protections under the UK Payment Services Regulations to these transactions, which helps to anchor trust in this new rail.

It also allows customers to benefit from faster and more transparent money flows. In many implementations, funds leave the customer’s account and arrive with the merchant in near real time, and refunds can be processed back to the bank account much more quickly than traditional card refunds. Customers keep a clear view of their spending directly in their bank statements, and can combine Pay by Bank with their existing bank security settings and alerts, giving a sense of control and visibility over each payment.

Across the UK payments landscape, the move is widely seen as one of the strongest endorsements yet of open banking and A2A payments by a global eCommerce leader, signalling that A2A is ready for prime-time in mainstream retail. By sidestepping card networks for some transactions, Amazon can reduce scheme and interchange fees and benefit from faster settlements, while banks and open banking providers gain a powerful proof-point for their infrastructure at scale.

If customer adoption grows, even a modest shift of Amazon’s UK volume from cards to Pay by Bank could meaningfully erode card share in eCommerce and prompt schemes, issuers and PSPs to sharpen pricing and differentiate more on value-added services such as instalments, rewards and advanced fraud controls. The launch also aligns with the UK’s National Payments Vision, which explicitly encourages A2A in eCommerce to deliver more efficient, secure and competitive payment options.

Giving the People What They Want

That strategic significance ultimately rests on customer behaviour.

Expanding payment options at checkout also aligns closely with evolving customer expectations in the UK, where research shows that a significant share of shoppers will abandon purchases if their preferred payment method is not available or the checkout journey feels cumbersome. UK consumers have rapidly adopted mobile and digital wallets, and there is growing comfort with open-banking payments, with a MoneyHub survey indicating that 45% of respondents feel comfortable using them for regular bills and 39% for larger transactions.

By adding a secure, bank-native option that fits seamlessly with modern mobile-banking habits and offers instant refunds and strong protections, Amazon is responding to this demand for more flexible, intuitive and trusted ways to pay online. In doing so, it not only enhances its own checkout but also raises the bar for what UK customers will expect from other merchants, potentially making a broader mix of cards, wallets and A2A Pay by Bank options the new norm across the market.

Key benefits for consumers include:

- Card details do not need to be entered or stored, increasing security.

- A familiar user experience as your mobile-banking app is used to authenticate via your PIN or preferred biometrics, increasing user trust.

- Faster refunds, with money returned to your bank account within minutes after Amazon confirms a return.

- No card expiry or card-detail updates, because the payment method is linked to your bank account rather than a physical card.

- Set up is incredibly quick and simple, and represents a low barrier to entry.

Wider Industry Effects

The sectors likely to feel the impact first are online retail and digital subscriptions, where transaction costs, authorisation rates and refund experiences are critical to margins and customer satisfaction. Amazon is initially enabling Pay by Bank for retail purchases on amazon.co.uk, and it claims the ability to pay for Prime membership is coming soon, directly challenging card-on-file in one of the UK’s flagship subscription products.

Over time, normalising Pay by Bank on such a large platform is expected to spill over into other verticals that are both digital-first and price-sensitive, including other marketplaces, travel and ticketing, utilities and telecoms, where merchants are already exploring open-banking A2A for bills and recurring payments. For PSPs, gateways and challenger acquirers, this creates a strong incentive to productise similar “pay from bank” buttons and instant-refund capabilities for their merchant bases, accelerating competition around A2A offerings.

As a Senior Research Analyst within Juniper Research’s Fintech and Payments team, Thomas provides up-to-date trends analysis, competitive landscape appraisals, and market sizing for financial markets. His most recent reports have covered areas including Digital Wallets, A2A Payments, and Digital Identity Verification.

Related Research

-

ReportSeptember 2025Fintech & Payments

ReportSeptember 2025Fintech & Payments Thomas WilsonA2A Payments Market, 2025-2030

Thomas WilsonA2A Payments Market, 2025-2030Our A2A Payments research suite provides detailed analysis of this rapidly changing market; enabling A2A payments service providers to gain an understanding of key payment trends and challenges, potential growth opportunities, and the competitive environment.

VIEW

Latest research, whitepapers & press releases

-

ReportApril 2026IoT & Emerging Technology

ReportApril 2026IoT & Emerging Technology Molly GatfordPhysical AI in Manufacturing & Logistics Market: 2026-2030

Molly GatfordPhysical AI in Manufacturing & Logistics Market: 2026-2030Our Physical AI in Manufacturing and Logistics research suite provides in-depth analysis of the key economic, operational, and technological factors driving growth in this fast-growing market.

VIEW -

ReportApril 2026Fintech & Payments

ReportApril 2026Fintech & Payments Nick MaynardAgentic Commerce Market: 2026-2031

Nick MaynardAgentic Commerce Market: 2026-2031Juniper Research’s Agentic Commerce research suite provides an insightful analysis of this rapidly emerging market; enabling stakeholders, including AI developers, payment infrastructure providers, eCommerce marketplaces, merchants and many others, to understand future growth, key trends, and the competitive environment.

VIEW -

ReportMarch 2026Fintech & Payments

ReportMarch 2026Fintech & Payments Michael GreenwoodB2B Payment Cards Market: 2026-2030

Michael GreenwoodB2B Payment Cards Market: 2026-2030Our B2B card payments research suite provides detailed analysis of this rapidly changing market; allowing B2B card providers to gain an understanding of key payment trends and challenges, potential growth opportunities, and the competitive environment.

VIEW -

ReportMarch 2026Telecoms & Connectivity

ReportMarch 2026Telecoms & Connectivity Alex WebbDirect Carrier Billing Market: 2026-2030

Alex WebbDirect Carrier Billing Market: 2026-2030Our Direct Carrier Billing research suite for mobile network operators provides detailed analysis and strategic recommendations for the direct carrier billing market over the next four years.

VIEW -

ReportMarch 2026Fintech & Payments

ReportMarch 2026Fintech & Payments Lorien CarterCross-border Payments Market: 2026-2030

Lorien CarterCross-border Payments Market: 2026-2030Our Cross-border Payments research suite provides a comprehensive and in-depth analysis of the evolving cross-border payments landscape; enabling stakeholders such as businesses, financial institutions, payment service providers, card networks, regulators, and technology infrastructure providers to understand future growth, key trends, and the competitive environment.

VIEW -

ReportFebruary 2026Telecoms & Connectivity

ReportFebruary 2026Telecoms & Connectivity Ardit BallhysaMobile Messaging Market: 2026-2030

Ardit BallhysaMobile Messaging Market: 2026-2030Juniper Research’s Mobile Messaging research suite provides mobile messaging vendors, mobile network operators, and enterprises with intelligence on how to capitalise on changing market dynamics within the mobile messaging market.

VIEW

-

WhitepaperApril 2026Fintech & Payments

Nick Maynard

WhitepaperApril 2026Fintech & Payments

Nick MaynardAgentic Commerce - Revolution or False Dawn?

Our complimentary whitepaper assesses the trends that are increasing agentic commerce adoption, and challenges to agentic commerce usage. Additionally, it includes a forecast summary of the global spend on agentic commerce by 2030.

VIEW -

WhitepaperMarch 2026Fintech & Payments

Michael Greenwood

WhitepaperMarch 2026Fintech & Payments

Michael GreenwoodHow B2B Payment Cards Are Streamlining Corporate Expenses

Our complimentary whitepaper, How B2B Payment Cards Are Streamlining Corporate Expenses, examines the state of the B2B payment cards market; considering its impact on different geographies and how it is shaping the modern B2B payments landscape through card controls, payment data analysis tools, and fully integrated spend management solutions.

VIEW -

WhitepaperMarch 2026Telecoms & Connectivity

Alex Webb

WhitepaperMarch 2026Telecoms & Connectivity

Alex WebbDirect Carrier Billing: Unlocking Emerging Revenue Streams for Operators

Our complimentary whitepaper, Direct Carrier Billing: Unlocking Emerging Revenue Streams for Operators, explores the emerging opportunities for mobile network operators to monetise direct carrier billing.

VIEW -

WhitepaperMarch 2026Telecoms & Connectivity

Molly Gatford

WhitepaperMarch 2026Telecoms & Connectivity

Molly GatfordMWC 2026: What's Next for Mobile?

Our latest whitepaper distils the most important announcements from MWC Barcelona 2026 and examines what they mean for the telecoms market over the year ahead. From network APIs and 5G monetisation to AI-RAN, direct-to-cell connectivity, and 5G-Advanced, it explains where the biggest opportunities — and challenges — will emerge next.

VIEW -

WhitepaperMarch 2026Fintech & Payments

Lorien Carter

WhitepaperMarch 2026Fintech & Payments

Lorien CarterThe Transformation of Cross-border Payment Infrastructure

Our complimentary whitepaper, The Transformation of Cross-border Payment Infrastructure, examines the state of the cross-border payments market; explaining the role of key actors in transforming the cross-border payment experience, as well as the current landscape and recent developments within the cross-border payments industry.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

Ardit Ballhysa

WhitepaperFebruary 2026Telecoms & Connectivity

Ardit BallhysaHow Social Media Will Disrupt Mobile Messaging Channels in 2026

Our complimentary whitepaper, How Social Media Will Disrupt Mobile Messaging Channels in 2026, explores the challenges and opportunities for operators and enterprises as social media traffic continues to increase.

VIEW

-

Fintech & Payments

Agentic Commerce Set to Generate $1.5 Trillion Globally by 2030, as Payments Infrastructure Leaders Revealed

April 2026 -

Fintech & Payments

B2B Card Payments to Reach $11 Trillion Globally in 2030, Accelerated by Increased Corporate Use

March 2026 -

Telecoms & Connectivity

Direct Carrier Billing to Grow by $35 Billion Globally Over the Next Four Years, as Anti-fraud Capabilities Are Enhanced by Network APIs

March 2026 -

Fintech & Payments

Sophisticated Microfinance Services Spend to Surpass $22 billion By 2030, as Mobile Money Services in Emerging Markets Mature

March 2026 -

Fintech & Payments

Top Three Global Leaders in Cross-border Payment Infrastructure Revealed

March 2026 -

Telecoms & Connectivity

MVNO Subscriber Revenue to Exceed $50 Billion Globally in 2030

March 2026