Stripe Expands Pay by Bank to France & Germany – But Can It Dethrone the Card?

Stripe, a global provider of payments software to businesses, has expanded its offering of account-to-account (A2A) payments to Germany and France through a continued partnership with TrueLayer, an Open Banking platform.

Stripe’s A2A product, called Pay by Bank, uses TrueLayer’s Open Banking infrastructure which connects bank accounts across Europe; enabling merchants to accept transactions directly from a customer’s bank account. This expansion follows the success of Stripe and TrueLayer partnering to offer the same service in the UK in September 2024. There is reason for Stripe to be optimistic about this expansion, with TrueLayer already processing €2 billion ($2.4 billion) of Pay by Bank transactions in France and €1.4 billion ($1.6 billion) in Germany.

Advantages of Pay by Bank

There are several advantages for merchants accepting payments by Pay by Bank over traditional payment methods.

One of the primary advantages is the lower transaction fees, especially when compared to card networks. The cost of card transaction fees is significant to businesses, as it is the most common form of consumer payments in the markets in which Stripe has so far launched Pay by Bank.

Another important advantage for merchants is the lack of chargebacks on Pay by Bank.

Chargebacks, both legitimate and fraudulent, represent a significant cost for many merchants. The large increase in fraudulent chargebacks in recent years has only increased the burden. Even when a fraudulent claim is beaten by a merchant, it takes time. This is a time when the merchant does not have access to the payments; interrupting cashflow which can push businesses to rely on financing, further increasing costs. Chargebacks also require a merchant to allocate resources to fight the chargeback, whether that is staff spending time putting together evidence, or the merchant spending money on a chargeback management platform to undertake this task.

Another benefit of Pay by Bank is its increased security. In the markets Stripe is targeting, there are clear Open Banking regulations, as well as the requirement for strong customer authentication from the Second Payment Services Directive (PSD2). These, together with the fact banks employ their own strong anti-fraud systems, mean that Pay by Bank is relatively resistant to fraud.

These advantages are more attractive to small and medium-sized enterprises (SMEs), as these costs represent a larger proportion of costs for merchants of this size, compared to large enterprises and multinationals who are more able to absorb the additional costs. As Stripe’s primary customer base are SMEs, this makes Pay by Bank a particularly valuable addition to its payments acceptance offering.

Another advantage for merchants is customer satisfaction, given the convenience that Pay by Bank provides. To pay using Pay by Bank online, the consumer simply has to select the Pay by Bank option at checkout and then verify their identity. This is quicker than manually entering payment card details and can be more secure as it can be verified using biometric verification. Likewise, refunded monies can be back in the customer’s bank account within seconds, minimising a too-often significant cause of frustration for consumers.

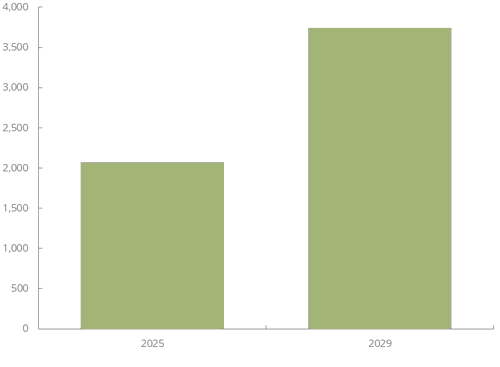

Juniper Research expects that these advantages will drive an 80% growth in the number of online A2A payments users between 2025 and 2029.

Total Global Online A2A Payment Users (m), 2025 vs. 2029

Source: Juniper Research

Challenges of Pay by Bank

Despite these advantages, Pay by Bank is not without its challenges.

The most significant challenge is consumer attitude. Many consumers are simply not aware of Pay by Bank as a payments option. Those who are aware of it may not fully understand what exactly it is or understand the advantages it offers over traditional payment methods. This compounds with consumers’ existing preference for card payments. Consumers are familiar with cards and trust them to be secure. There is also consumer protection in place, in markets such as the UK; ensuring that consumers get their money back if they are a victim of fraud that was not their fault. This makes any security advantages of Pay by Bank less of a concern for consumers.

Another disadvantage of Pay by Bank, compared to credit cards, is its inability to extend lines of credit or offer rewards for its use. This means those who use credit cards are very unlikely to give up these benefits for the additional convenience of using Pay by Bank.

A limitation of the payment method is its reliance on Open Banking regulation to enable it, without needing to partner with the consumer’s bank. Without Open Banking, the process of enabling Pay by Bank is significantly complicated, and banks’ unwillingness to partner to allow this can significantly restrict coverage. This means Pay by Bank is unlikely to gain much traction in any market that does not have Open Banking regulations to support this payment method.

Another challenge is facilitating cross-border transactions using Pay by Bank. Due to Pay by Bank’s reliance on regulations facilitating the payment method, there are markets, such as the US, where merchants are less likely to accept it. Equally, for merchants that have many international customers, a proportion of these customers will not have Pay by Bank supported in their country. This contrasts with the major card networks, where merchants will have customers in nearly every market and facilitate cross-border transactions between them regularly. This is not an issue within the EU, as all countries have the same Open Banking regulation, as do other countries which have signed up for regulatory alignment.

Pay by Bank is gaining traction in markets where the regulatory framework is in place. Partnerships, such as the one between Stripe and TrueLayer, will further boost this payment method, with it becoming easier for merchants to accept these payments. Juniper Research expects that Pay by Bank will continue to grow over the coming years, especially if Pay by Bank providers focus on raising awareness among consumers. However, it will be quite some time before it becomes a true competitor to the major card networks.

As a Senior Research Analyst, Michael delivers in-depth insights into the fast-evolving worlds of digital identity and payments. His recent work spans critical topics such as Digital Wallets, Digital Identity, and Instant Payments; helping industry leaders navigate change and identify new opportunities.

Related Research

-

ReportSeptember 2025Fintech & Payments

ReportSeptember 2025Fintech & Payments Thomas WilsonA2A Payments Market, 2025-2030

Thomas WilsonA2A Payments Market, 2025-2030Our A2A Payments research suite provides detailed analysis of this rapidly changing market; enabling A2A payments service providers to gain an understanding of key payment trends and challenges, potential growth opportunities, and the competitive environment.

VIEW -

ReportFebruary 2025Open Banking APIs

ReportFebruary 2025Open Banking APIs Matthew PurnellOpen Banking APIs Market, 2025-2029

Matthew PurnellOpen Banking APIs Market, 2025-2029Our Global Open Banking APIs research suite provides detailed and perceptive analysis of this evolving market; enabling stakeholders such as Open Banking infrastructure and payment service providers, banks and other financial institutions, and eCommerce platforms and merchants to understand future growth, key trends, and the competitive environment.

VIEW

Latest research, whitepapers & press releases

-

ReportAugust 2026Fintech & Payments

ReportAugust 2026Fintech & Payments Nick MaynardContactless Payments Market Data: 2026-2031

Nick MaynardContactless Payments Market Data: 2026-2031Our Contactless Payments market analysis provides exhaustive data coverage of the market in its entirety, including the adoption of mobile wallets featuring contactless payment technology, the growth of contactless transactions, and the market’s associated values.

VIEW -

ReportAugust 2026Fintech & Payments

Nick MaynardDigital Ticketing Market Data: 2026-2031

ReportAugust 2026Fintech & Payments

Nick MaynardDigital Ticketing Market Data: 2026-2031Our Digital Ticketing report provides exhaustive coverage of the digital ticketing market, including the adoption rates of digital ticketing across different ticketing segments, as well as the use of wearable payments and chatbots.

VIEW -

ReportAugust 2026Fintech & Payments

Nick MaynardQR Code Payments Market: 2026-2031

ReportAugust 2026Fintech & Payments

Nick MaynardQR Code Payments Market: 2026-2031This research provides exhaustive coverage of the QR Code Payments market, including the adoption rates of QR code payment systems across retail, person-to-person (P2P), and ticketing use cases.

VIEW -

ReportJuly 2026IoT & Emerging Technology

ReportJuly 2026IoT & Emerging Technology Saffron DusanjhVLEO Satellite Market: 2026-2031

Saffron DusanjhVLEO Satellite Market: 2026-2031Our Very Low Earth Orbit (VLEO) Satellite Market research suite provides comprehensive analysis of one of the fastest-emerging markets within the global space economy.

VIEW -

ReportJuly 2026Telecoms & Connectivity

ReportJuly 2026Telecoms & Connectivity Alex WebbIPX Providers Competitor Leaderboard: 2026

Alex WebbIPX Providers Competitor Leaderboard: 2026Our IPX Providers Competitor Leaderboard 2026 delivers comprehensive evaluation and examination of 16 leading IPX vendors. It provides mobile network operators and other IPX customers with profiles, competitor benchmarking, and strategic analysis of these leading providers.

VIEW -

ReportJuly 2026Fintech & Payments

ReportJuly 2026Fintech & Payments Jawad JahanPOS Market: 2026-2031

Jawad JahanPOS Market: 2026-2031Our Point of Sale (POS) Market research suite provides detailed and insightful analysis of this evolving market; enabling stakeholders - from POS hardware manufacturers, payment infrastructure providers, software developers, and hospitality and retail vendors - to understand future growth, key trends, and the competitive environment.

VIEW

-

WhitepaperJuly 2026IoT & Emerging Technology

Saffron Dusanjh

WhitepaperJuly 2026IoT & Emerging Technology

Saffron DusanjhBeyond LEO: Why VLEO is Becoming the Next Growth Market

Our complimentary whitepaper, Beyond LEO: Why VLEO is Becoming the Next Growth Market, explores how VLEO is transitioning from an experimental orbital regime into a commercially viable market.

VIEW -

WhitepaperJuly 2026Fintech & Payments

Jawad Jahan

WhitepaperJuly 2026Fintech & Payments

Jawad JahanFrom Transaction to Transformation: The Future of POS

Our complimentary whitepaper, From Transaction to Transformation: The Future of POS, analyses the current landscape of the POS market. It also provides insight into key trends shaping the POS market, such as POS terminals increasingly being used as a business management platform.

VIEW -

WhitepaperJuly 2026Fintech & Payments

WhitepaperJuly 2026Fintech & Payments Shane O'Sullivan

Shane O'SullivanBeyond the Boarding Pass: The Digital Travel Credential Paradigm

Our complimentary whitepaper, Beyond the Boarding Pass: The Digital Travel Credential Paradigm, examines the rapidly evolving state of the digital travel credential market.

VIEW -

WhitepaperJuly 2026Fintech & Payments

WhitepaperJuly 2026Fintech & Payments Thomas Wilson

Thomas WilsonThe Top Three Drivers of Network Tokenisation Adoption

Our complimentary whitepaper, The Top Three Drivers of Network Tokenisation Adoption, examines the state of the network tokenisation market; considering its impact on different payment modalities, how it is shaping the modern payments landscape through safer, more secure payments, and how it could unlock the potential of agentic commerce.

VIEW -

WhitepaperJune 2026Fintech & Payments

Nick Maynard

WhitepaperJune 2026Fintech & Payments

Nick MaynardMoney20/20 Europe 2026 Key Takeaways: What You Need to Know Post-event

Money 20/20 Europe once again brought together people from across the fintech, payments and identity ecosystems; creating three days of discussions, announcements and networking.

VIEW -

WhitepaperJune 2026Fintech & Payments

WhitepaperJune 2026Fintech & Payments Michael Greenwood

Michael GreenwoodChargeback Management: The Fightback Against Friendly Fraud

Our complimentary whitepaper, Chargeback Management: The Fightback Against Friendly Fraud, examines the growing impact of friendly fraud on the chargeback management space, as well as how chargeback management tools are mitigating this threat.

VIEW

-

IoT & Emerging Technology

VLEO Satellites: Global Investment to Near $10 Billion by 2031; Driven by Falling Launch Costs

July 2026 -

Telecoms & Connectivity

Juniper Research Identifies Syniverse, BICS, and iBASIS as Leaders in the IPX Market

July 2026 -

Fintech & Payments

POS Transactions to Reach $41 Trillion Globally by 2031, as Convergence Towards Unified Commerce Surges

July 2026 -

Fintech & Payments

Digital Travel Credentials: 1.2 Billion Passengers to Adopt DTCs Globally by 2035, Fuelled by Passenger Demand for Seamless Journeys

July 2026 -

Fintech & Payments

Network Tokenisation to Secure 2.4 Trillion Global Transactions Between 2026 and 2030 – Representing 86% of Applicable Transactions

July 2026 -

Telecoms & Connectivity

Juniper Research Identifies BICS, Telna, and Vodafone Procure & Connect as Leaders in the Sponsored Roaming Market

July 2026