AWS Outage: Are Enterprises Overestimating Cloud Reliability?

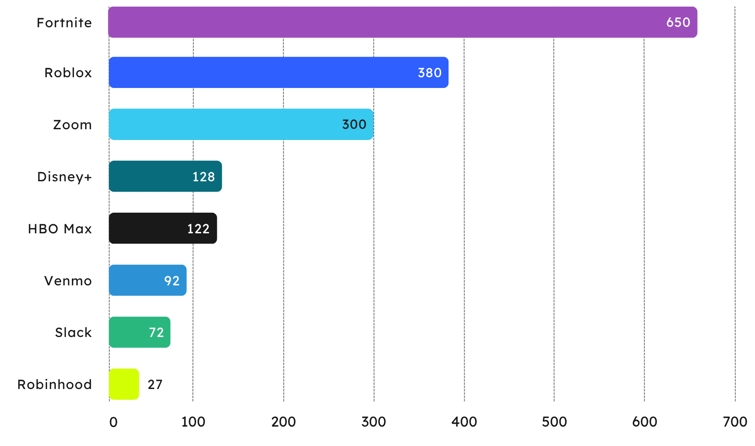

On October 20th, 2025, Amazon Web Services (AWS) experienced a substantial outage of its services in the US, with global impacts. The outage, caused by a domain name system (DNS) resolution failure that impacted a key database service, resulted in a cascading effect on AWS services. In turn, this led to many services that rely on AWS to also suffer outages; impacting consumers of various services including Disney+, Fortnite, HBO Max, Robinhood, Roblox, Slack, Venmo, and Zoom.

Estimated User Base for Select Service Providers Impacted by AWS Outage (m)

Source: Juniper Research

While AWS resolved the root cause of the issue within three hours, there were substantial impacts on various enterprises that leverage AWS. Despite the disruption, Amazon’s stock remained relatively stable; suggesting continued investor confidence in the company’s long-term market leadership. However, the incident could accelerate demand for multi-cloud orchestration tools, edge computing, and services that increase the overall resilience of cloud services. Overall, we expect the outage to initiate enterprises to explore new solutions or business models to increase the uptime of their services.

Is There an Overreliance on One Provider for Cloud Services?

The short answer is yes, we believe that there is an overreliance on many cloud services, notably AWS — which Juniper Research estimates to have a global market share of over 30%. As a company that has such a noteworthy presence in the market, it attracts the highest spending enterprises through significant degrees of redundancy within their operations to avoid scenarios like this. However, as is evident, no service is perfectly redundant, especially as the geographical reach of cloud services offered increases the complexity of network architectures. The larger the cloud service becomes, there is more within the service to fail, and a larger chance for cascading failures.

While AWS offers service credits for downtime, it does not cover the full operational and reputational costs. The event serves as a reminder that even leading cloud providers are not immune to large-scale disruptions.

Lessons are to be learned from this outage. Enterprises must not believe that services from AWS, and other leading providers such as Google and Microsoft, can be wholly relied upon, especially for enterprises that operate across multiple regions. The impacts of a failed DNS resolution must lead enterprises to explore multi-cloud strategies to increase redundancy and avoid vendor lock-in. Additionally, we recommend that enterprises implement their own monitoring software and not rely on the services provided by cloud providers.

The Financial Impact of AWS’s Outage

The financial impact of the outage is difficult to quantify at this stage, but we believe it will be significant. Many fintech services, such as Robinhood and Venmo, suffered downtime on their own platforms, which will likely lead to time spent on chargeback and dispute resolution, plus indirect costs of the outage. Similarly, digital platforms providers such as Disney+ and HBO Max suffered service interruptions; albeit for a small amount of downtime.

Aside from direct revenue loss from downtime, such as missed transactions and halted services, several indirect losses have resulted from this outage:

- Lost productivity for users of services such as Zoom or Slack. Many other enterprises rely on this for internal and external communication. This causes delays to AWS clients.

- Disrupted operations caused by the outage can also cause indirect costs through lost time. Key examples of this are enterprises in the healthcare or aviation industries that must be considered time-sensitive industries, where efficiency is key to maintaining profit; notably as profit margins can be small.

- Loss to brand reputation if services are down for substantial periods; leading to high levels of customer dissatisfaction. Essentially, this loss is unquantifiable, given the subjectivity and changes to opinion over time.

- Customer compensation, particularly in sectors like finance, travel, and telecoms, can add further costs through required refunds and service credits — as well as the unexpected time and resource needed to complete them.

How Must the Market Respond to this Outage?

It is reported that AWS’s service level agreements (SLAs) include 99.99% uptime for virtual servers, with discounts or credits to future services if AWS fails to meet these requirements. However, it's unlikely that these agreements cover lost enterprise revenue, productivity or reputational damage. Therefore, an enterprise’s choice of cloud service provider, or providers, must consider the impacts of this kind of outage. We believe that outages of any service are inevitable at some point.

Adopting a multi-cloud strategy will increase resilience and allow enterprises to mitigate the risks, direct costs, and indirect costs associated with these outages. A multi-cloud strategy will increase resilience and minimise the risk of extended periods of service downtime by enabling fallback onto a secondary service provider.

However, a key hurdle to enterprise adoption of multi-cloud strategies is the increased cost and complexity of implementation. For example, cloud service vendors will use a different suite of APIs, and security processes and functions are not interoperable between different platforms. Not only does this strategy lead to increased spend on cloud platforms, but additional training on the additional cloud service.

Outages such as this are a clear reminder that no service provider, regardless of reputation, scale or reach, can guarantee 100% uptime or provide complete protection against service downtime. While multi-vendor strategies will increase resilience, the high cost and interoperability challenges involved will likely exclude most cloud service users from adopting this strategy.

Indeed, we believe that cloud providers should embrace this challenge; providing solutions that are interoperable with other cloud platforms, including network APIs, to maximise the value of their solutions to enterprise users. After this outage, Juniper Research expects increased interest in a multi-cloud strategy, and platforms that can reduce spend and investment into integrating with additional systems will increase their value proposition to enterprises.

As VP of Telecoms Market Research at Juniper Research, Sam produces high-quality research on telecommunications technologies and the future of digital content. His recent reports include CPaaS, Direct-to-Cell, and 5G Future Strategies. Sam has been interviewed by leading media outlets, including the BBC and Wall Street Journal, and is a regular contributor to messaging conferences and telecommunications industry events.

Related Research

-

ReportAugust 2025Telecoms & Connectivity

ReportAugust 2025Telecoms & Connectivity Alex WebbNetwork APIs Market, 2025-2030

Alex WebbNetwork APIs Market, 2025-2030Our Network API research suite provides operators, CPaaS providers, and other GSMA channel partners with extensive analysis and actionable insights into the rapidly growing network API market. It contains data that allows stakeholders in the market to make informed decisions on their product development and business strategies in the network API market.

VIEW -

ReportMay 2024Telecoms & Connectivity

Alex WebbTelecommunications Cloud Strategies Market, 2024-2028

ReportMay 2024Telecoms & Connectivity

Alex WebbTelecommunications Cloud Strategies Market, 2024-2028Our Telecommunications Cloud research suite provides actionable insights and analysis into this rapidly growing and competitive market; enabling stakeholders, such as operators, cloud providers, network equipment providers, and hyperscalers to navigate and capitalise on the development of cloud infrastructure in telecommunications networks.

VIEW -

ReportMay 2025Telecoms & Connectivity

ReportMay 2025Telecoms & Connectivity Fred SavageOperator Revenue Strategies, 2025-2029

Fred SavageOperator Revenue Strategies, 2025-2029Discover invaluable insights into trends and strategies for network operator revenue in our latest report, Network Operator Revenue Strategies. With data split across 60 countries, this extensive forecast analyses the dynamic and competitive network operator market and the current market challenges posed by slowing revenue, high market saturation in the consumer market, rising network ownership costs, and challenges in 5G monetisation.

VIEW

Latest research, whitepapers & press releases

-

ReportAugust 2026Fintech & Payments

ReportAugust 2026Fintech & Payments Nick MaynardContactless Payments Market Data: 2026-2031

Nick MaynardContactless Payments Market Data: 2026-2031Our Contactless Payments market analysis provides exhaustive data coverage of the market in its entirety, including the adoption of mobile wallets featuring contactless payment technology, the growth of contactless transactions, and the market’s associated values.

VIEW -

ReportAugust 2026Fintech & Payments

Nick MaynardDigital Ticketing Market Data: 2026-2031

ReportAugust 2026Fintech & Payments

Nick MaynardDigital Ticketing Market Data: 2026-2031Our Digital Ticketing report provides exhaustive coverage of the digital ticketing market, including the adoption rates of digital ticketing across different ticketing segments, as well as the use of wearable payments and chatbots.

VIEW -

ReportAugust 2026Fintech & Payments

Nick MaynardQR Code Payments Market: 2026-2031

ReportAugust 2026Fintech & Payments

Nick MaynardQR Code Payments Market: 2026-2031This research provides exhaustive coverage of the QR Code Payments market, including the adoption rates of QR code payment systems across retail, person-to-person (P2P), and ticketing use cases.

VIEW -

ReportJuly 2026IoT & Emerging Technology

ReportJuly 2026IoT & Emerging Technology Saffron DusanjhVLEO Satellite Market: 2026-2031

Saffron DusanjhVLEO Satellite Market: 2026-2031Our Very Low Earth Orbit (VLEO) Satellite Market research suite provides comprehensive analysis of one of the fastest-emerging markets within the global space economy.

VIEW -

ReportJuly 2026Telecoms & Connectivity

ReportJuly 2026Telecoms & Connectivity Alex WebbIPX Providers Competitor Leaderboard: 2026

Alex WebbIPX Providers Competitor Leaderboard: 2026Our IPX Providers Competitor Leaderboard 2026 delivers comprehensive evaluation and examination of 16 leading IPX vendors. It provides mobile network operators and other IPX customers with profiles, competitor benchmarking, and strategic analysis of these leading providers.

VIEW -

ReportJuly 2026Fintech & Payments

ReportJuly 2026Fintech & Payments Jawad JahanPOS Market: 2026-2031

Jawad JahanPOS Market: 2026-2031Our Point of Sale (POS) Market research suite provides detailed and insightful analysis of this evolving market; enabling stakeholders - from POS hardware manufacturers, payment infrastructure providers, software developers, and hospitality and retail vendors - to understand future growth, key trends, and the competitive environment.

VIEW

-

WhitepaperJuly 2026IoT & Emerging Technology

Saffron Dusanjh

WhitepaperJuly 2026IoT & Emerging Technology

Saffron DusanjhBeyond LEO: Why VLEO is Becoming the Next Growth Market

Our complimentary whitepaper, Beyond LEO: Why VLEO is Becoming the Next Growth Market, explores how VLEO is transitioning from an experimental orbital regime into a commercially viable market.

VIEW -

WhitepaperJuly 2026Fintech & Payments

Jawad Jahan

WhitepaperJuly 2026Fintech & Payments

Jawad JahanFrom Transaction to Transformation: The Future of POS

Our complimentary whitepaper, From Transaction to Transformation: The Future of POS, analyses the current landscape of the POS market. It also provides insight into key trends shaping the POS market, such as POS terminals increasingly being used as a business management platform.

VIEW -

WhitepaperJuly 2026Fintech & Payments

WhitepaperJuly 2026Fintech & Payments Shane O'Sullivan

Shane O'SullivanBeyond the Boarding Pass: The Digital Travel Credential Paradigm

Our complimentary whitepaper, Beyond the Boarding Pass: The Digital Travel Credential Paradigm, examines the rapidly evolving state of the digital travel credential market.

VIEW -

WhitepaperJuly 2026Fintech & Payments

WhitepaperJuly 2026Fintech & Payments Thomas Wilson

Thomas WilsonThe Top Three Drivers of Network Tokenisation Adoption

Our complimentary whitepaper, The Top Three Drivers of Network Tokenisation Adoption, examines the state of the network tokenisation market; considering its impact on different payment modalities, how it is shaping the modern payments landscape through safer, more secure payments, and how it could unlock the potential of agentic commerce.

VIEW -

WhitepaperJune 2026Fintech & Payments

Nick Maynard

WhitepaperJune 2026Fintech & Payments

Nick MaynardMoney20/20 Europe 2026 Key Takeaways: What You Need to Know Post-event

Money 20/20 Europe once again brought together people from across the fintech, payments and identity ecosystems; creating three days of discussions, announcements and networking.

VIEW -

WhitepaperJune 2026Fintech & Payments

WhitepaperJune 2026Fintech & Payments Michael Greenwood

Michael GreenwoodChargeback Management: The Fightback Against Friendly Fraud

Our complimentary whitepaper, Chargeback Management: The Fightback Against Friendly Fraud, examines the growing impact of friendly fraud on the chargeback management space, as well as how chargeback management tools are mitigating this threat.

VIEW

-

Telecoms & Connectivity

Conversational AI Usage to Surge by 88% Globally by 2030; Driven by Rich Media Channels

August 2026 -

Fintech & Payments

Chargeback Requests to Surge to 616 Million Globally by 2031; Driving Demand for Automated Chargeback Management Solutions

August 2026 -

Fintech & Payments

Contact-free Payments Become the Default as Contactless Transactions Exceed $32 Trillion Globally by 2031

August 2026 -

IoT & Emerging Technology

VLEO Satellites: Global Investment to Near $10 Billion by 2031; Driven by Falling Launch Costs

July 2026 -

Telecoms & Connectivity

Juniper Research Identifies Syniverse, BICS, and iBASIS as Leaders in the IPX Market

July 2026 -

Fintech & Payments

POS Transactions to Reach $41 Trillion Globally by 2031, as Convergence Towards Unified Commerce Surges

July 2026