AWS Outage: Are Enterprises Overestimating Cloud Reliability?

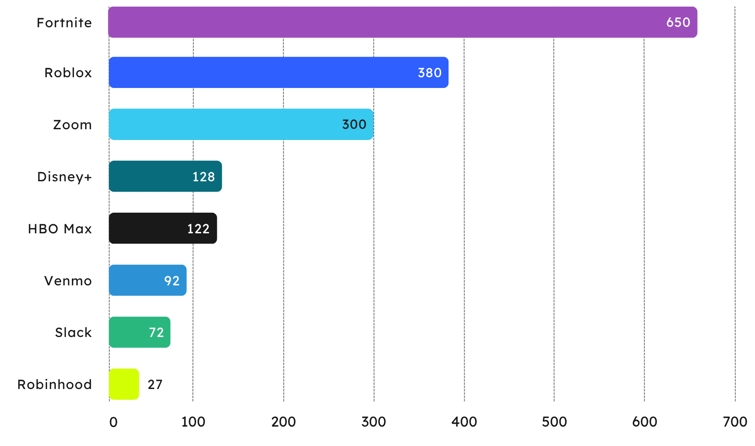

On October 20th, 2025, Amazon Web Services (AWS) experienced a substantial outage of its services in the US, with global impacts. The outage, caused by a domain name system (DNS) resolution failure that impacted a key database service, resulted in a cascading effect on AWS services. In turn, this led to many services that rely on AWS to also suffer outages; impacting consumers of various services including Disney+, Fortnite, HBO Max, Robinhood, Roblox, Slack, Venmo, and Zoom.

Estimated User Base for Select Service Providers Impacted by AWS Outage (m)

Source: Juniper Research

While AWS resolved the root cause of the issue within three hours, there were substantial impacts on various enterprises that leverage AWS. Despite the disruption, Amazon’s stock remained relatively stable; suggesting continued investor confidence in the company’s long-term market leadership. However, the incident could accelerate demand for multi-cloud orchestration tools, edge computing, and services that increase the overall resilience of cloud services. Overall, we expect the outage to initiate enterprises to explore new solutions or business models to increase the uptime of their services.

Is There an Overreliance on One Provider for Cloud Services?

The short answer is yes, we believe that there is an overreliance on many cloud services, notably AWS — which Juniper Research estimates to have a global market share of over 30%. As a company that has such a noteworthy presence in the market, it attracts the highest spending enterprises through significant degrees of redundancy within their operations to avoid scenarios like this. However, as is evident, no service is perfectly redundant, especially as the geographical reach of cloud services offered increases the complexity of network architectures. The larger the cloud service becomes, there is more within the service to fail, and a larger chance for cascading failures.

While AWS offers service credits for downtime, it does not cover the full operational and reputational costs. The event serves as a reminder that even leading cloud providers are not immune to large-scale disruptions.

Lessons are to be learned from this outage. Enterprises must not believe that services from AWS, and other leading providers such as Google and Microsoft, can be wholly relied upon, especially for enterprises that operate across multiple regions. The impacts of a failed DNS resolution must lead enterprises to explore multi-cloud strategies to increase redundancy and avoid vendor lock-in. Additionally, we recommend that enterprises implement their own monitoring software and not rely on the services provided by cloud providers.

The Financial Impact of AWS’s Outage

The financial impact of the outage is difficult to quantify at this stage, but we believe it will be significant. Many fintech services, such as Robinhood and Venmo, suffered downtime on their own platforms, which will likely lead to time spent on chargeback and dispute resolution, plus indirect costs of the outage. Similarly, digital platforms providers such as Disney+ and HBO Max suffered service interruptions; albeit for a small amount of downtime.

Aside from direct revenue loss from downtime, such as missed transactions and halted services, several indirect losses have resulted from this outage:

- Lost productivity for users of services such as Zoom or Slack. Many other enterprises rely on this for internal and external communication. This causes delays to AWS clients.

- Disrupted operations caused by the outage can also cause indirect costs through lost time. Key examples of this are enterprises in the healthcare or aviation industries that must be considered time-sensitive industries, where efficiency is key to maintaining profit; notably as profit margins can be small.

- Loss to brand reputation if services are down for substantial periods; leading to high levels of customer dissatisfaction. Essentially, this loss is unquantifiable, given the subjectivity and changes to opinion over time.

- Customer compensation, particularly in sectors like finance, travel, and telecoms, can add further costs through required refunds and service credits — as well as the unexpected time and resource needed to complete them.

How Must the Market Respond to this Outage?

It is reported that AWS’s service level agreements (SLAs) include 99.99% uptime for virtual servers, with discounts or credits to future services if AWS fails to meet these requirements. However, it's unlikely that these agreements cover lost enterprise revenue, productivity or reputational damage. Therefore, an enterprise’s choice of cloud service provider, or providers, must consider the impacts of this kind of outage. We believe that outages of any service are inevitable at some point.

Adopting a multi-cloud strategy will increase resilience and allow enterprises to mitigate the risks, direct costs, and indirect costs associated with these outages. A multi-cloud strategy will increase resilience and minimise the risk of extended periods of service downtime by enabling fallback onto a secondary service provider.

However, a key hurdle to enterprise adoption of multi-cloud strategies is the increased cost and complexity of implementation. For example, cloud service vendors will use a different suite of APIs, and security processes and functions are not interoperable between different platforms. Not only does this strategy lead to increased spend on cloud platforms, but additional training on the additional cloud service.

Outages such as this are a clear reminder that no service provider, regardless of reputation, scale or reach, can guarantee 100% uptime or provide complete protection against service downtime. While multi-vendor strategies will increase resilience, the high cost and interoperability challenges involved will likely exclude most cloud service users from adopting this strategy.

Indeed, we believe that cloud providers should embrace this challenge; providing solutions that are interoperable with other cloud platforms, including network APIs, to maximise the value of their solutions to enterprise users. After this outage, Juniper Research expects increased interest in a multi-cloud strategy, and platforms that can reduce spend and investment into integrating with additional systems will increase their value proposition to enterprises.

As VP of Telecoms Market Research at Juniper Research, Sam produces high-quality research on telecommunications technologies and the future of digital content. His recent reports include CPaaS, Direct-to-Cell, and 5G Future Strategies. Sam has been interviewed by leading media outlets, including the BBC and Wall Street Journal, and is a regular contributor to messaging conferences and telecommunications industry events.

Related Research

-

ReportAugust 2025Telecoms & Connectivity

ReportAugust 2025Telecoms & Connectivity Alex Webb

Alex WebbNetwork APIs Market, 2025-2030

Our Network API research suite provides operators, CPaaS providers, and other GSMA channel partners with extensive analysis and actionable insights into the rapidly growing network API market. It contains data that allows stakeholders in the market to make informed decisions on their product development and business strategies in the network API market.

VIEW -

ReportMay 2024Telecoms & Connectivity

Alex Webb

ReportMay 2024Telecoms & Connectivity

Alex WebbTelecommunications Cloud Strategies Market, 2024-2028

Our Telecommunications Cloud research suite provides actionable insights and analysis into this rapidly growing and competitive market; enabling stakeholders, such as operators, cloud providers, network equipment providers, and hyperscalers to navigate and capitalise on the development of cloud infrastructure in telecommunications networks.

VIEW -

ReportMay 2025Telecoms & Connectivity

ReportMay 2025Telecoms & Connectivity Fred Savage

Fred SavageOperator Revenue Strategies, 2025-2029

Discover invaluable insights into trends and strategies for network operator revenue in our latest report, Network Operator Revenue Strategies. With data split across 60 countries, this extensive forecast analyses the dynamic and competitive network operator market and the current market challenges posed by slowing revenue, high market saturation in the consumer market, rising network ownership costs, and challenges in 5G monetisation.

VIEW

Latest research, whitepapers & press releases

-

ReportFebruary 2026Telecoms & Connectivity

ReportFebruary 2026Telecoms & Connectivity Ardit BallhysaMobile Messaging Market: 2026-2030

Ardit BallhysaMobile Messaging Market: 2026-2030Juniper Research’s Mobile Messaging research suite provides mobile messaging vendors, mobile network operators, and enterprises with intelligence on how to capitalise on changing market dynamics within the mobile messaging market.

VIEW -

ReportFebruary 2026Fintech & Payments

ReportFebruary 2026Fintech & Payments Shane O'SullivanKYC/KYB Systems Market: 2026-2030

Shane O'SullivanKYC/KYB Systems Market: 2026-2030Our KYC/KYB Systems research suite provides a detailed and insightful analysis of an evolving market; enabling stakeholders such as financial institutions, eCommerce platforms, regulatory agencies and technology vendors to understand future growth, key trends and the competitive environment.

VIEW -

ReportFebruary 2026Telecoms & Connectivity

ReportFebruary 2026Telecoms & Connectivity Molly GatfordRCS for Business: 2026-2030

Molly GatfordRCS for Business: 2026-2030Our comprehensive RCS for Business research suite provides an in‑depth evaluation of a market poised for rapid expansion over the next five years. It equips stakeholders with clear insight into the most significant opportunities emerging over the next two years.

VIEW -

ReportFebruary 2026Fintech & Payments

ReportFebruary 2026Fintech & Payments Jawad JahanMobile Money in Emerging Markets: 2026-2030

Jawad JahanMobile Money in Emerging Markets: 2026-2030Our Mobile Money in Emerging Markets research report provides detailed evaluation and analysis of the ways in which the mobile financial services space is evolving and developing.

VIEW -

ReportJanuary 2026IoT & Emerging Technology

ReportJanuary 2026IoT & Emerging Technology Louis AtkinPost-quantum Cryptography Market: 2026-2035

Louis AtkinPost-quantum Cryptography Market: 2026-2035Juniper Research’s Post-quantum Cryptography (PQC) research suite provides a comprehensive and insightful analysis of this market; enabling stakeholders, including PQC-enabled platform providers, specialists, cybersecurity consultancies, and many others, to understand future growth, key trends, and the competitive environment.

VIEW -

ReportJanuary 2026Telecoms & Connectivity

ReportJanuary 2026Telecoms & Connectivity Alex WebbMVNO in a Box Market: 2026-2030

Alex WebbMVNO in a Box Market: 2026-2030Juniper Research’s MVNO in a Box research suite provides Mobile Virtual Network Enablers, Mobile Virtual Network Aggregators, and other players with detailed analysis and strategic recommendations for monetising demand for MVNO in a Box services.

VIEW

-

WhitepaperFebruary 2026Telecoms & Connectivity

Ardit Ballhysa

WhitepaperFebruary 2026Telecoms & Connectivity

Ardit BallhysaHow Social Media Will Disrupt Mobile Messaging Channels in 2026

Our complimentary whitepaper, How Social Media Will Disrupt Mobile Messaging Channels in 2026, explores the challenges and opportunities for operators and enterprises as social media traffic continues to increase.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

WhitepaperFebruary 2026Telecoms & Connectivity Sam Barker

Sam BarkerProtecting Users from Scam Ads: A Call for Social Media Platform Accountability

In this new whitepaper commissioned by Revolut, Juniper Research examines how scam advertising has become embedded across major social media platforms, quantifies the scale of user exposure and financial harm, and explains why current detection and enforcement measures are failing to keep pace.

VIEW -

WhitepaperFebruary 2026Fintech & Payments

Shane O'Sullivan

WhitepaperFebruary 2026Fintech & Payments

Shane O'SullivanKnow Your Agents (KYA): The Next Frontier in KYC/KYB Systems

Our complimentary whitepaper, Know Your Agents (KYA): The Next Frontier in KYC/KYB Systems, examines the state of the KYC/KYB systems market; considering the impact of regulatory development, emerging risk factors such as identity enabled fraud, and how identity and business verification is evolving beyond traditional customer and merchant onboarding toward agent-level governance.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

Molly Gatford

WhitepaperFebruary 2026Telecoms & Connectivity

Molly Gatford3 Key Strategies for Capitalising on RCS Growth in 2026

Our complimentary whitepaper, 3 Key Strategies for Capitalising on RCS Growth in 2026, explores key trends shaping the RCS for Business market and outlines how mobile operators and platforms can accelerate adoption and maximise revenue over the next 12 months.

VIEW -

WhitepaperFebruary 2026Fintech & Payments

Jawad Jahan

WhitepaperFebruary 2026Fintech & Payments

Jawad JahanThe Next Steps for Mobile Money – Interoperability and Openness

Our complimentary whitepaper, The Next Steps for Mobile Money – Interoperability and Openness, analyses how interoperability and open platforms can drive new growth opportunities through partnerships with key stakeholders.

VIEW -

WhitepaperJanuary 2026IoT & Emerging Technology

Louis Atkin

WhitepaperJanuary 2026IoT & Emerging Technology

Louis AtkinPreparing for Q-Day: Post-quantum Security Shift

Our complimentary whitepaper, Preparing for Q-Day: Post-quantum Security Shift, assesses the factors which are increasing interest in adopting PQC, and challenges to PQC adoption. Additionally, it includes a forecast summary of the global spend on PQC by 2035.

VIEW

-

Telecoms & Connectivity

MVNO Subscriber Revenue to Exceed $50 Billion Globally in 2030

March 2026 -

Fintech & Payments

QUBE Events is excited to bring back the 24th NextGen Payments & RegTech Forum - Switzerland

February 2026 -

Telecoms & Connectivity

OTT Messaging Apps to Exceed 5 Billion Users Globally by 2028; Driving Shift in Enterprise Communication Strategies

February 2026 -

Fintech & Payments

Calling All Fintech & Payment Innovators: Future Digital Awards Now Open for 2026

February 2026 -

Telecoms & Connectivity

Operator RCS for Business Revenue to Reach $3 Billion Globally by 2027, Growing 150% in Two Years

February 2026 -

Fintech & Payments

KYC & KYB Systems Spend Outside Financial Sector to Grow 105% by 2030 Globally, as KYC Moves Beyond Banking

February 2026