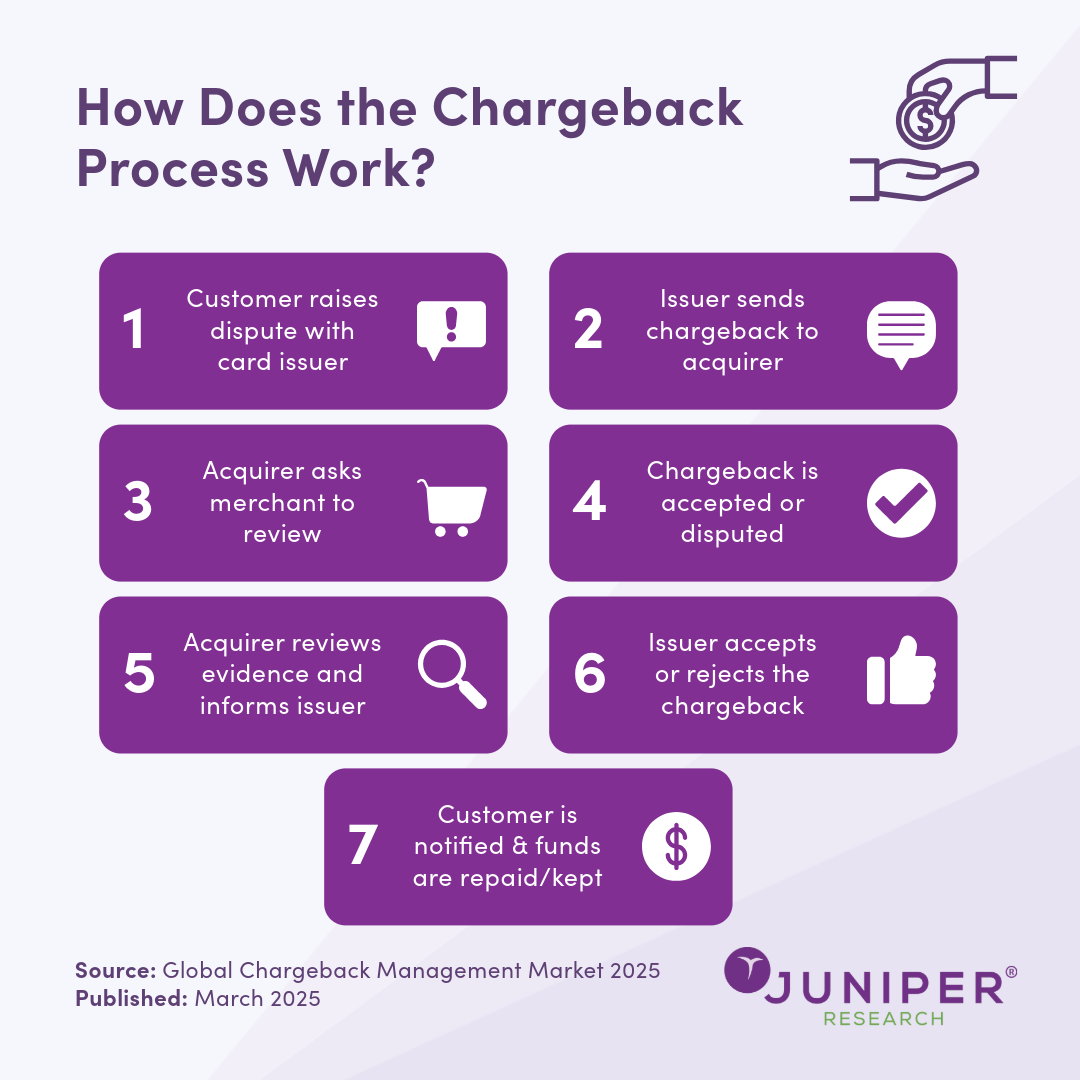

Understanding the Chargeback Process: Types & Challenges

Chargebacks were originally designed to help customers reverse transactions when they’ve fallen victim to fraud. This can include scenarios such as stolen cards, payment credentials, or account takeovers. However, before issuing a chargeback, customers are expected to try all other options with the merchant, such as requesting a refund.

There are three primary situations that lead to chargebacks:

- Legitimate chargebacks: These occur when a customer is defrauded by a third party, such as when their card details are stolen and used without their knowledge. In these cases, chargebacks function as intended, protecting consumers from unauthorised transactions.

- Erroneous chargebacks: This happens when a customer mistakenly believes a transaction was fraudulent, often due to a misunderstanding of their transaction history. Subscription services frequently experience this issue when customers forget about ongoing payments or fail to recognise a merchant name on their statement.

- Chargeback/friendly fraud: This occurs when a customer intentionally requests a chargeback for a legitimate transaction, even though they agreed to the terms and conditions at the time of purchase. This can range from buyer’s remorse to outright abuse of the chargeback system.

While these categories may seem straightforward, the issue of chargebacks is far more complex than it appears. Initially created to combat fraud, chargebacks have evolved into a tool for customers to resolve disputes with merchants, even when fraud isn’t involved. In some industries, chargebacks are increasingly being used in ways that go beyond their intended purpose.

For example, in hospitality, customers may raise chargebacks when they are billed for additional fees they agreed to, such as charges for bringing a pet into a hotel room or smoking in a non-smoking room. Similarly, in digital services and eCommerce, customers may dispute charges for non-refundable bookings, digital content, or online courses - even after accessing or using the service.

This shift in customer perception has made chargebacks an increasingly challenging issue for merchants across various industries. High chargeback rates can lead to financial losses, increased payment processing fees, and even penalties from card networks if chargeback thresholds are exceeded.

As digital payments continue to evolve, so too will the chargeback landscape. Merchants that take a proactive approach - combining fraud prevention, customer education, and robust dispute management - will be better positioned to minimise chargeback losses and maintain strong customer relationships.

Chargebacks aren’t going away, but with the right strategies, businesses can stay ahead of the challenge.

Source: Global Chargeback Management Market 2025

Download the Whitepaper: Fighting Friendly Fraud with Chargeback Management Systems

Read the Press Release: Chargeback Management: Which Companies Will Lead the Market in 2025?

Latest research, whitepapers & press releases

-

ReportMarch 2026Fintech & Payments

ReportMarch 2026Fintech & Payments Lorien CarterCross-border Payments Market: 2026-2030

Lorien CarterCross-border Payments Market: 2026-2030Our Cross-border Payments research suite provides a comprehensive and in-depth analysis of the evolving cross-border payments landscape; enabling stakeholders such as businesses, financial institutions, payment service providers, card networks, regulators, and technology infrastructure providers to understand future growth, key trends, and the competitive environment.

VIEW -

ReportFebruary 2026Telecoms & Connectivity

ReportFebruary 2026Telecoms & Connectivity Ardit BallhysaMobile Messaging Market: 2026-2030

Ardit BallhysaMobile Messaging Market: 2026-2030Juniper Research’s Mobile Messaging research suite provides mobile messaging vendors, mobile network operators, and enterprises with intelligence on how to capitalise on changing market dynamics within the mobile messaging market.

VIEW -

ReportFebruary 2026Fintech & Payments

ReportFebruary 2026Fintech & Payments Shane O'SullivanKYC/KYB Systems Market: 2026-2030

Shane O'SullivanKYC/KYB Systems Market: 2026-2030Our KYC/KYB Systems research suite provides a detailed and insightful analysis of an evolving market; enabling stakeholders such as financial institutions, eCommerce platforms, regulatory agencies and technology vendors to understand future growth, key trends and the competitive environment.

VIEW -

ReportFebruary 2026Telecoms & Connectivity

ReportFebruary 2026Telecoms & Connectivity Molly GatfordRCS for Business Market: 2026-2030

Molly GatfordRCS for Business Market: 2026-2030Our comprehensive RCS for Business research suite provides an in‑depth evaluation of a market poised for rapid expansion over the next five years. It equips stakeholders with clear insight into the most significant opportunities emerging over the next two years.

VIEW -

ReportFebruary 2026Fintech & Payments

ReportFebruary 2026Fintech & Payments Jawad JahanMobile Money in Emerging Markets: 2026-2030

Jawad JahanMobile Money in Emerging Markets: 2026-2030Our Mobile Money in Emerging Markets research report provides detailed evaluation and analysis of the ways in which the mobile financial services space is evolving and developing.

VIEW -

ReportJanuary 2026IoT & Emerging Technology

ReportJanuary 2026IoT & Emerging Technology Louis AtkinPost-quantum Cryptography Market: 2026-2035

Louis AtkinPost-quantum Cryptography Market: 2026-2035Juniper Research’s Post-quantum Cryptography (PQC) research suite provides a comprehensive and insightful analysis of this market; enabling stakeholders, including PQC-enabled platform providers, specialists, cybersecurity consultancies, and many others, to understand future growth, key trends, and the competitive environment.

VIEW

-

WhitepaperMarch 2026Telecoms & Connectivity

Molly Gatford

WhitepaperMarch 2026Telecoms & Connectivity

Molly GatfordMWC 2026: What's Next for Mobile?

Our latest whitepaper distils the most important announcements from MWC Barcelona 2026 and examines what they mean for the telecoms market over the year ahead. From network APIs and 5G monetisation to AI-RAN, direct-to-cell connectivity, and 5G-Advanced, it explains where the biggest opportunities — and challenges — will emerge next.

VIEW -

WhitepaperMarch 2026Fintech & Payments

Lorien Carter

WhitepaperMarch 2026Fintech & Payments

Lorien CarterThe Transformation of Cross-border Payment Infrastructure

Our complimentary whitepaper, The Transformation of Cross-border Payment Infrastructure, examines the state of the cross-border payments market; explaining the role of key actors in transforming the cross-border payment experience, as well as the current landscape and recent developments within the cross-border payments industry.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

Ardit Ballhysa

WhitepaperFebruary 2026Telecoms & Connectivity

Ardit BallhysaHow Social Media Will Disrupt Mobile Messaging Channels in 2026

Our complimentary whitepaper, How Social Media Will Disrupt Mobile Messaging Channels in 2026, explores the challenges and opportunities for operators and enterprises as social media traffic continues to increase.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

WhitepaperFebruary 2026Telecoms & Connectivity Sam Barker

Sam BarkerProtecting Users from Scam Ads: A Call for Social Media Platform Accountability

In this new whitepaper commissioned by Revolut, Juniper Research examines how scam advertising has become embedded across major social media platforms, quantifies the scale of user exposure and financial harm, and explains why current detection and enforcement measures are failing to keep pace.

VIEW -

WhitepaperFebruary 2026Fintech & Payments

Shane O'Sullivan

WhitepaperFebruary 2026Fintech & Payments

Shane O'SullivanKnow Your Agents (KYA): The Next Frontier in KYC/KYB Systems

Our complimentary whitepaper, Know Your Agents (KYA): The Next Frontier in KYC/KYB Systems, examines the state of the KYC/KYB systems market; considering the impact of regulatory development, emerging risk factors such as identity enabled fraud, and how identity and business verification is evolving beyond traditional customer and merchant onboarding toward agent-level governance.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

Molly Gatford

WhitepaperFebruary 2026Telecoms & Connectivity

Molly Gatford3 Key Strategies for Capitalising on RCS Growth in 2026

Our complimentary whitepaper, 3 Key Strategies for Capitalising on RCS Growth in 2026, explores key trends shaping the RCS for Business market and outlines how mobile operators and platforms can accelerate adoption and maximise revenue over the next 12 months.

VIEW

-

Fintech & Payments

Top Three Global Leaders in Cross-border Payment Infrastructure Revealed

March 2026 -

Telecoms & Connectivity

MVNO Subscriber Revenue to Exceed $50 Billion Globally in 2030

March 2026 -

Fintech & Payments

QUBE Events is excited to bring back the 24th NextGen Payments & RegTech Forum - Switzerland

February 2026 -

Telecoms & Connectivity

OTT Messaging Apps to Exceed 5 Billion Users Globally by 2028; Driving Shift in Enterprise Communication Strategies

February 2026 -

Fintech & Payments

Calling All Fintech & Payment Innovators: Future Digital Awards Now Open for 2026

February 2026 -

Telecoms & Connectivity

Operator RCS for Business Revenue to Reach $3 Billion Globally by 2027, Growing 150% in Two Years

February 2026