The Future of Payments: What’s Powering the A2A Boom?

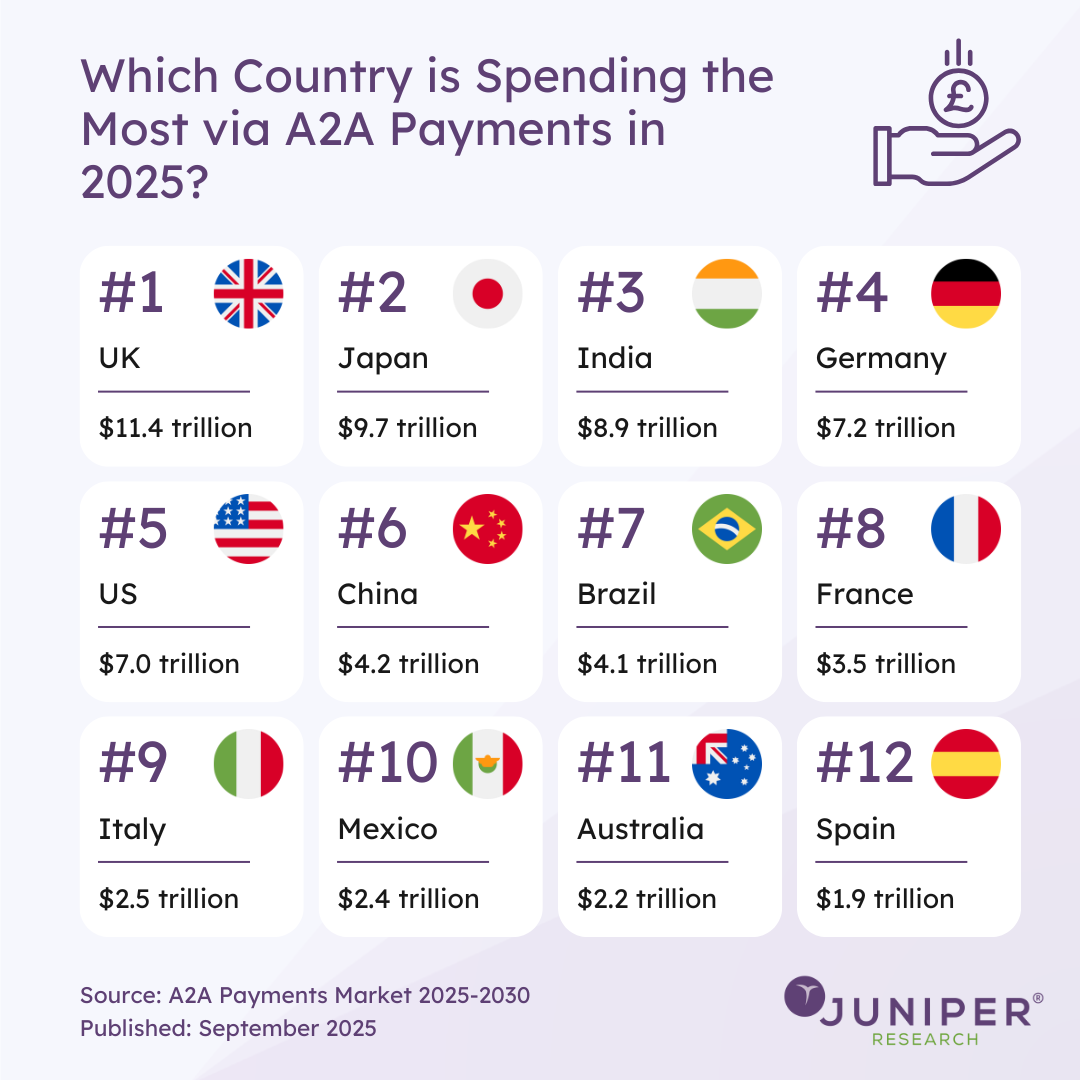

Account-to-Account (A2A) payments are no longer a niche option. By 2025, spending via A2A will hit staggering levels – with the UK leading the way at $11.4 trillion, followed closely by Japan and India. But what’s behind this rapid rise? Several factors are converging to make A2A payments one of the most significant shifts in financial services today.

The Role of Technology

Smartphones have become the backbone of modern finance, enabling consumers to send and receive money with just a few taps. Features such as biometric authentication and QR code scanning make A2A payments seamless, while app-based requests simplify everything from peer-to-peer (P2P) transfers to online shopping.

Artificial intelligence is also reshaping the landscape. AI-driven fraud detection, behavioural biometrics, and automated verification processes mean that A2A payments are now both more secure and more convenient. This combination of speed and safety is essential for winning consumer trust.

Government Initiatives and Regulation

National payment schemes have been instrumental in driving adoption. India’s UPI and Brazil’s Pix are prime examples of how government-backed infrastructure can revolutionise everyday payments. Similarly, the EU’s adoption of ISO 20022 has set global standards for interoperability, making it easier for businesses and consumers to embrace A2A.

Meanwhile, Open Banking initiatives are unlocking new possibilities such as Variable Recurring Payments (VRPs), which give consumers more control over subscriptions and regular payments. This level of regulatory support is pushing A2A into the mainstream across multiple regions.

Lower Costs, Better Cash Flow

For businesses, one of the biggest draws is cost. Traditional wire transfers can be expensive, with fees ranging from $0 to $50 per transaction in the US, plus hefty surcharges on international transfers. By contrast, A2A payments via systems like FedNow can cost just a few cents per transaction.

By cutting out intermediaries such as card networks, A2A payments help businesses manage cash flow more effectively. Funds settle instantly, reducing reconciliation delays and operational costs. For consumers, these savings often translate into lower fees and smoother payment experiences.

Expanding Financial Inclusion

A2A payments are also helping to close the financial inclusion gap. In emerging markets, QR code–based payments allow even small businesses or unbanked individuals to participate in digital commerce with nothing more than a smartphone and internet access.

By lowering barriers to entry, A2A is enabling broader participation in digital financial systems. This not only benefits individuals in remote or underserved communities but also supports local economic development.

Building Consumer Trust

Security remains central to A2A adoption. Strong Customer Authentication (SCA) requirements, combined with multi-factor authentication, have dramatically reduced fraud rates. Enhanced transparency – such as real-time confirmation of payment transfers – further builds user confidence.

Providers are also innovating with refund processes and protections, ensuring that consumers feel as secure with A2A as they do with card-based payments.

Source: A2A Payments Market 2025-2030

Read the Press Release: A2A Transaction Value to Reach $195 Trillion in 2030 Globally, Driven by Advanced Value-added Services

Download the Whitepaper: Ascending-to-Ailing: The Deceleration of A2A Adoption

Latest research, whitepapers & press releases

-

ReportMarch 2026Fintech & Payments

ReportMarch 2026Fintech & Payments Lorien CarterCross-border Payments Market: 2026-2030

Lorien CarterCross-border Payments Market: 2026-2030Our Cross-border Payments research suite provides a comprehensive and in-depth analysis of the evolving cross-border payments landscape; enabling stakeholders such as businesses, financial institutions, payment service providers, card networks, regulators, and technology infrastructure providers to understand future growth, key trends, and the competitive environment.

VIEW -

ReportFebruary 2026Telecoms & Connectivity

ReportFebruary 2026Telecoms & Connectivity Ardit BallhysaMobile Messaging Market: 2026-2030

Ardit BallhysaMobile Messaging Market: 2026-2030Juniper Research’s Mobile Messaging research suite provides mobile messaging vendors, mobile network operators, and enterprises with intelligence on how to capitalise on changing market dynamics within the mobile messaging market.

VIEW -

ReportFebruary 2026Fintech & Payments

ReportFebruary 2026Fintech & Payments Shane O'SullivanKYC/KYB Systems Market: 2026-2030

Shane O'SullivanKYC/KYB Systems Market: 2026-2030Our KYC/KYB Systems research suite provides a detailed and insightful analysis of an evolving market; enabling stakeholders such as financial institutions, eCommerce platforms, regulatory agencies and technology vendors to understand future growth, key trends and the competitive environment.

VIEW -

ReportFebruary 2026Telecoms & Connectivity

ReportFebruary 2026Telecoms & Connectivity Molly GatfordRCS for Business Market: 2026-2030

Molly GatfordRCS for Business Market: 2026-2030Our comprehensive RCS for Business research suite provides an in‑depth evaluation of a market poised for rapid expansion over the next five years. It equips stakeholders with clear insight into the most significant opportunities emerging over the next two years.

VIEW -

ReportFebruary 2026Fintech & Payments

ReportFebruary 2026Fintech & Payments Jawad JahanMobile Money in Emerging Markets: 2026-2030

Jawad JahanMobile Money in Emerging Markets: 2026-2030Our Mobile Money in Emerging Markets research report provides detailed evaluation and analysis of the ways in which the mobile financial services space is evolving and developing.

VIEW -

ReportJanuary 2026IoT & Emerging Technology

ReportJanuary 2026IoT & Emerging Technology Louis AtkinPost-quantum Cryptography Market: 2026-2035

Louis AtkinPost-quantum Cryptography Market: 2026-2035Juniper Research’s Post-quantum Cryptography (PQC) research suite provides a comprehensive and insightful analysis of this market; enabling stakeholders, including PQC-enabled platform providers, specialists, cybersecurity consultancies, and many others, to understand future growth, key trends, and the competitive environment.

VIEW

-

WhitepaperMarch 2026Telecoms & Connectivity

Molly Gatford

WhitepaperMarch 2026Telecoms & Connectivity

Molly GatfordMWC 2026: What's Next for Mobile?

Our latest whitepaper distils the most important announcements from MWC Barcelona 2026 and examines what they mean for the telecoms market over the year ahead. From network APIs and 5G monetisation to AI-RAN, direct-to-cell connectivity, and 5G-Advanced, it explains where the biggest opportunities — and challenges — will emerge next.

VIEW -

WhitepaperMarch 2026Fintech & Payments

Lorien Carter

WhitepaperMarch 2026Fintech & Payments

Lorien CarterThe Transformation of Cross-border Payment Infrastructure

Our complimentary whitepaper, The Transformation of Cross-border Payment Infrastructure, examines the state of the cross-border payments market; explaining the role of key actors in transforming the cross-border payment experience, as well as the current landscape and recent developments within the cross-border payments industry.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

Ardit Ballhysa

WhitepaperFebruary 2026Telecoms & Connectivity

Ardit BallhysaHow Social Media Will Disrupt Mobile Messaging Channels in 2026

Our complimentary whitepaper, How Social Media Will Disrupt Mobile Messaging Channels in 2026, explores the challenges and opportunities for operators and enterprises as social media traffic continues to increase.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

WhitepaperFebruary 2026Telecoms & Connectivity Sam Barker

Sam BarkerProtecting Users from Scam Ads: A Call for Social Media Platform Accountability

In this new whitepaper commissioned by Revolut, Juniper Research examines how scam advertising has become embedded across major social media platforms, quantifies the scale of user exposure and financial harm, and explains why current detection and enforcement measures are failing to keep pace.

VIEW -

WhitepaperFebruary 2026Fintech & Payments

Shane O'Sullivan

WhitepaperFebruary 2026Fintech & Payments

Shane O'SullivanKnow Your Agents (KYA): The Next Frontier in KYC/KYB Systems

Our complimentary whitepaper, Know Your Agents (KYA): The Next Frontier in KYC/KYB Systems, examines the state of the KYC/KYB systems market; considering the impact of regulatory development, emerging risk factors such as identity enabled fraud, and how identity and business verification is evolving beyond traditional customer and merchant onboarding toward agent-level governance.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

Molly Gatford

WhitepaperFebruary 2026Telecoms & Connectivity

Molly Gatford3 Key Strategies for Capitalising on RCS Growth in 2026

Our complimentary whitepaper, 3 Key Strategies for Capitalising on RCS Growth in 2026, explores key trends shaping the RCS for Business market and outlines how mobile operators and platforms can accelerate adoption and maximise revenue over the next 12 months.

VIEW

-

Fintech & Payments

Sophisticated Microfinance Services Spend to Surpass $22 billion By 2030, as Mobile Money Services in Emerging Markets Mature

March 2026 -

Fintech & Payments

Top Three Global Leaders in Cross-border Payment Infrastructure Revealed

March 2026 -

Telecoms & Connectivity

MVNO Subscriber Revenue to Exceed $50 Billion Globally in 2030

March 2026 -

Fintech & Payments

QUBE Events is excited to bring back the 24th NextGen Payments & RegTech Forum - Switzerland

February 2026 -

Telecoms & Connectivity

OTT Messaging Apps to Exceed 5 Billion Users Globally by 2028; Driving Shift in Enterprise Communication Strategies

February 2026 -

Fintech & Payments

Calling All Fintech & Payment Innovators: Future Digital Awards Now Open for 2026

February 2026