Stripe Expands Pay by Bank to France & Germany – But Can It Dethrone the Card?

Stripe, a global provider of payments software to businesses, has expanded its offering of account-to-account (A2A) payments to Germany and France through a continued partnership with TrueLayer, an Open Banking platform.

Stripe’s A2A product, called Pay by Bank, uses TrueLayer’s Open Banking infrastructure which connects bank accounts across Europe; enabling merchants to accept transactions directly from a customer’s bank account. This expansion follows the success of Stripe and TrueLayer partnering to offer the same service in the UK in September 2024. There is reason for Stripe to be optimistic about this expansion, with TrueLayer already processing €2 billion ($2.4 billion) of Pay by Bank transactions in France and €1.4 billion ($1.6 billion) in Germany.

Advantages of Pay by Bank

There are several advantages for merchants accepting payments by Pay by Bank over traditional payment methods.

One of the primary advantages is the lower transaction fees, especially when compared to card networks. The cost of card transaction fees is significant to businesses, as it is the most common form of consumer payments in the markets in which Stripe has so far launched Pay by Bank.

Another important advantage for merchants is the lack of chargebacks on Pay by Bank.

Chargebacks, both legitimate and fraudulent, represent a significant cost for many merchants. The large increase in fraudulent chargebacks in recent years has only increased the burden. Even when a fraudulent claim is beaten by a merchant, it takes time. This is a time when the merchant does not have access to the payments; interrupting cashflow which can push businesses to rely on financing, further increasing costs. Chargebacks also require a merchant to allocate resources to fight the chargeback, whether that is staff spending time putting together evidence, or the merchant spending money on a chargeback management platform to undertake this task.

Another benefit of Pay by Bank is its increased security. In the markets Stripe is targeting, there are clear Open Banking regulations, as well as the requirement for strong customer authentication from the Second Payment Services Directive (PSD2). These, together with the fact banks employ their own strong anti-fraud systems, mean that Pay by Bank is relatively resistant to fraud.

These advantages are more attractive to small and medium-sized enterprises (SMEs), as these costs represent a larger proportion of costs for merchants of this size, compared to large enterprises and multinationals who are more able to absorb the additional costs. As Stripe’s primary customer base are SMEs, this makes Pay by Bank a particularly valuable addition to its payments acceptance offering.

Another advantage for merchants is customer satisfaction, given the convenience that Pay by Bank provides. To pay using Pay by Bank online, the consumer simply has to select the Pay by Bank option at checkout and then verify their identity. This is quicker than manually entering payment card details and can be more secure as it can be verified using biometric verification. Likewise, refunded monies can be back in the customer’s bank account within seconds, minimising a too-often significant cause of frustration for consumers.

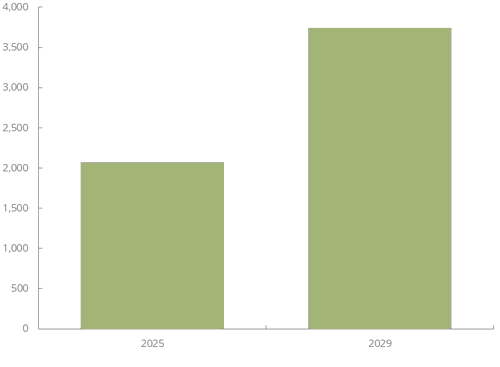

Juniper Research expects that these advantages will drive an 80% growth in the number of online A2A payments users between 2025 and 2029.

Total Global Online A2A Payment Users (m), 2025 vs. 2029

Source: Juniper Research

Challenges of Pay by Bank

Despite these advantages, Pay by Bank is not without its challenges.

The most significant challenge is consumer attitude. Many consumers are simply not aware of Pay by Bank as a payments option. Those who are aware of it may not fully understand what exactly it is or understand the advantages it offers over traditional payment methods. This compounds with consumers’ existing preference for card payments. Consumers are familiar with cards and trust them to be secure. There is also consumer protection in place, in markets such as the UK; ensuring that consumers get their money back if they are a victim of fraud that was not their fault. This makes any security advantages of Pay by Bank less of a concern for consumers.

Another disadvantage of Pay by Bank, compared to credit cards, is its inability to extend lines of credit or offer rewards for its use. This means those who use credit cards are very unlikely to give up these benefits for the additional convenience of using Pay by Bank.

A limitation of the payment method is its reliance on Open Banking regulation to enable it, without needing to partner with the consumer’s bank. Without Open Banking, the process of enabling Pay by Bank is significantly complicated, and banks’ unwillingness to partner to allow this can significantly restrict coverage. This means Pay by Bank is unlikely to gain much traction in any market that does not have Open Banking regulations to support this payment method.

Another challenge is facilitating cross-border transactions using Pay by Bank. Due to Pay by Bank’s reliance on regulations facilitating the payment method, there are markets, such as the US, where merchants are less likely to accept it. Equally, for merchants that have many international customers, a proportion of these customers will not have Pay by Bank supported in their country. This contrasts with the major card networks, where merchants will have customers in nearly every market and facilitate cross-border transactions between them regularly. This is not an issue within the EU, as all countries have the same Open Banking regulation, as do other countries which have signed up for regulatory alignment.

Pay by Bank is gaining traction in markets where the regulatory framework is in place. Partnerships, such as the one between Stripe and TrueLayer, will further boost this payment method, with it becoming easier for merchants to accept these payments. Juniper Research expects that Pay by Bank will continue to grow over the coming years, especially if Pay by Bank providers focus on raising awareness among consumers. However, it will be quite some time before it becomes a true competitor to the major card networks.

As a Senior Research Analyst, Michael delivers in-depth insights into the fast-evolving worlds of digital identity and payments. His recent work spans critical topics such as Digital Wallets, Digital Identity, and Instant Payments; helping industry leaders navigate change and identify new opportunities.

Related Research

-

ReportSeptember 2025Fintech & Payments

ReportSeptember 2025Fintech & Payments Thomas WilsonA2A Payments Market, 2025-2030

Thomas WilsonA2A Payments Market, 2025-2030Our A2A Payments research suite provides detailed analysis of this rapidly changing market; enabling A2A payments service providers to gain an understanding of key payment trends and challenges, potential growth opportunities, and the competitive environment.

VIEW -

ReportFebruary 2025Open Banking APIs

ReportFebruary 2025Open Banking APIs Matthew PurnellOpen Banking APIs Market, 2025-2029

Matthew PurnellOpen Banking APIs Market, 2025-2029Our Global Open Banking APIs research suite provides detailed and perceptive analysis of this evolving market; enabling stakeholders such as Open Banking infrastructure and payment service providers, banks and other financial institutions, and eCommerce platforms and merchants to understand future growth, key trends, and the competitive environment.

VIEW

Latest research, whitepapers & press releases

-

ReportMarch 2026Fintech & Payments

ReportMarch 2026Fintech & Payments Lorien CarterCross-border Payments Market: 2026-2030

Lorien CarterCross-border Payments Market: 2026-2030Our Cross-border Payments research suite provides a comprehensive and in-depth analysis of the evolving cross-border payments landscape; enabling stakeholders such as businesses, financial institutions, payment service providers, card networks, regulators, and technology infrastructure providers to understand future growth, key trends, and the competitive environment.

VIEW -

ReportFebruary 2026Telecoms & Connectivity

ReportFebruary 2026Telecoms & Connectivity Ardit BallhysaMobile Messaging Market: 2026-2030

Ardit BallhysaMobile Messaging Market: 2026-2030Juniper Research’s Mobile Messaging research suite provides mobile messaging vendors, mobile network operators, and enterprises with intelligence on how to capitalise on changing market dynamics within the mobile messaging market.

VIEW -

ReportFebruary 2026Fintech & Payments

ReportFebruary 2026Fintech & Payments Shane O'SullivanKYC/KYB Systems Market: 2026-2030

Shane O'SullivanKYC/KYB Systems Market: 2026-2030Our KYC/KYB Systems research suite provides a detailed and insightful analysis of an evolving market; enabling stakeholders such as financial institutions, eCommerce platforms, regulatory agencies and technology vendors to understand future growth, key trends and the competitive environment.

VIEW -

ReportFebruary 2026Telecoms & Connectivity

ReportFebruary 2026Telecoms & Connectivity Molly GatfordRCS for Business Market: 2026-2030

Molly GatfordRCS for Business Market: 2026-2030Our comprehensive RCS for Business research suite provides an in‑depth evaluation of a market poised for rapid expansion over the next five years. It equips stakeholders with clear insight into the most significant opportunities emerging over the next two years.

VIEW -

ReportFebruary 2026Fintech & Payments

ReportFebruary 2026Fintech & Payments Jawad JahanMobile Money in Emerging Markets: 2026-2030

Jawad JahanMobile Money in Emerging Markets: 2026-2030Our Mobile Money in Emerging Markets research report provides detailed evaluation and analysis of the ways in which the mobile financial services space is evolving and developing.

VIEW -

ReportJanuary 2026IoT & Emerging Technology

ReportJanuary 2026IoT & Emerging Technology Louis AtkinPost-quantum Cryptography Market: 2026-2035

Louis AtkinPost-quantum Cryptography Market: 2026-2035Juniper Research’s Post-quantum Cryptography (PQC) research suite provides a comprehensive and insightful analysis of this market; enabling stakeholders, including PQC-enabled platform providers, specialists, cybersecurity consultancies, and many others, to understand future growth, key trends, and the competitive environment.

VIEW

-

WhitepaperMarch 2026Telecoms & Connectivity

Molly Gatford

WhitepaperMarch 2026Telecoms & Connectivity

Molly GatfordMWC 2026: What's Next for Mobile?

Our latest whitepaper distils the most important announcements from MWC Barcelona 2026 and examines what they mean for the telecoms market over the year ahead. From network APIs and 5G monetisation to AI-RAN, direct-to-cell connectivity, and 5G-Advanced, it explains where the biggest opportunities — and challenges — will emerge next.

VIEW -

WhitepaperMarch 2026Fintech & Payments

Lorien Carter

WhitepaperMarch 2026Fintech & Payments

Lorien CarterThe Transformation of Cross-border Payment Infrastructure

Our complimentary whitepaper, The Transformation of Cross-border Payment Infrastructure, examines the state of the cross-border payments market; explaining the role of key actors in transforming the cross-border payment experience, as well as the current landscape and recent developments within the cross-border payments industry.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

Ardit Ballhysa

WhitepaperFebruary 2026Telecoms & Connectivity

Ardit BallhysaHow Social Media Will Disrupt Mobile Messaging Channels in 2026

Our complimentary whitepaper, How Social Media Will Disrupt Mobile Messaging Channels in 2026, explores the challenges and opportunities for operators and enterprises as social media traffic continues to increase.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

WhitepaperFebruary 2026Telecoms & Connectivity Sam Barker

Sam BarkerProtecting Users from Scam Ads: A Call for Social Media Platform Accountability

In this new whitepaper commissioned by Revolut, Juniper Research examines how scam advertising has become embedded across major social media platforms, quantifies the scale of user exposure and financial harm, and explains why current detection and enforcement measures are failing to keep pace.

VIEW -

WhitepaperFebruary 2026Fintech & Payments

Shane O'Sullivan

WhitepaperFebruary 2026Fintech & Payments

Shane O'SullivanKnow Your Agents (KYA): The Next Frontier in KYC/KYB Systems

Our complimentary whitepaper, Know Your Agents (KYA): The Next Frontier in KYC/KYB Systems, examines the state of the KYC/KYB systems market; considering the impact of regulatory development, emerging risk factors such as identity enabled fraud, and how identity and business verification is evolving beyond traditional customer and merchant onboarding toward agent-level governance.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

Molly Gatford

WhitepaperFebruary 2026Telecoms & Connectivity

Molly Gatford3 Key Strategies for Capitalising on RCS Growth in 2026

Our complimentary whitepaper, 3 Key Strategies for Capitalising on RCS Growth in 2026, explores key trends shaping the RCS for Business market and outlines how mobile operators and platforms can accelerate adoption and maximise revenue over the next 12 months.

VIEW

-

Fintech & Payments

Sophisticated Microfinance Services Spend to Surpass $22 billion By 2030, as Mobile Money Services in Emerging Markets Mature

March 2026 -

Fintech & Payments

Top Three Global Leaders in Cross-border Payment Infrastructure Revealed

March 2026 -

Telecoms & Connectivity

MVNO Subscriber Revenue to Exceed $50 Billion Globally in 2030

March 2026 -

Fintech & Payments

QUBE Events is excited to bring back the 24th NextGen Payments & RegTech Forum - Switzerland

February 2026 -

Telecoms & Connectivity

OTT Messaging Apps to Exceed 5 Billion Users Globally by 2028; Driving Shift in Enterprise Communication Strategies

February 2026 -

Fintech & Payments

Calling All Fintech & Payment Innovators: Future Digital Awards Now Open for 2026

February 2026