Is 2025 the Year of Digital ID in the UK?

The UK is a market often noted for its resistance to digital ID or national identity systems in general. It is often believed that the UK public are less open to the idea than citizens of other countries and prioritise privacy over the efficiency gains a digital ID system could offer. However, this is slowly changing, as indicated by a YouGov poll in December 2024 which found strong support for a system of national identity cards in the UK.

Question: Would you support or oppose the introduction of a

system of national identity cards in Britain?

Source: YouGov

Another significant movement in December 2024 occurred with the unveiling of new proposed legislation that, if passed, would enable UK residents to use digital IDs to verify their age when buying alcohol. This will be applicable in pubs, clubs, and shops. The IDs will be provided by third-party companies and checked against government records, with these checks carried out by either NFC or QR codes, ensuring the process is streamlined. These digital IDs will also not reveal the user’s name or address, as is the case with traditional IDs.

These changes will come from the Data (Use and Access) Bill, introduced to Parliament in 2024. The bill is currently in the House of Lords, with it still needing to pass the House of Commons and gain Royal Assent before it becomes law. In its press release, the Department for Science, Innovation and Technology state they expect it to be in force by the end of 2025.

This follows on from the 2023 decision, by the previous government, to allow UK citizens to upload identity documents to apps in order to carry out Disclosure and Barring Service (DBS), right to work, and right to rent checks. These services are provided by third-party identity services, such as Yoti, and it is expected that the same companies will be involved in the provision of the new digital IDs.

Source: Yoti

It is worth stressing that this will be a fairly limited programme, with participation entirely optional for both consumers and businesses. This will likely result in slow and uneven adoption, as was seen with the 2023 roll-out of digital IDs, with the vast majority of locations which accepted these IDs being in London or other major cities. This is due to the fact that consumers are unlikely to adopt the technology unless it is usable in a good number of the locations they use. Equally, businesses are less likely to adopt it if consumers are not using it. This results in the market for these technologies taking longer to reach critical mass and become widespread.

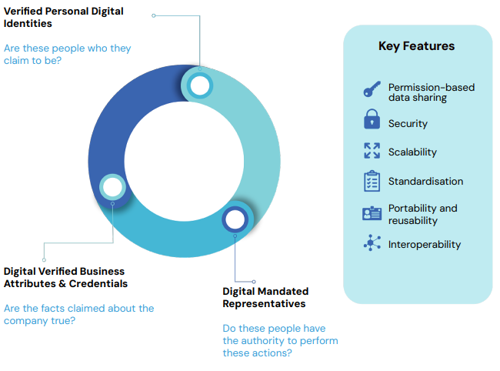

It is not only in the consumer sector that digital identity is growing in the UK. In December 2024, a coalition of leading financial institutions and technology companies, led by the UK’s Centre for Finance and Innovation Technology (CFIT), unveiled their progress on designing a digital company ID.

Proposed Components of 'Digital Company ID'

Source: CFIT

The proposed model would enable CFIT to create a working prototype, in the form of a virtual passport for businesses. CFIT suggest that the widespread adoption of a digital company ID would help prevent fraud, boost efficiencies for banks and other financial institutions. This work was supported by the Chancellor, in the National Payments Vision published in November 2024, with the document pledging to ‘consider any finding that emerge from CFIT’s work in due course’. CFIT will announce the results, recommendations and next steps from its programme in March 2025.

The adoption of digital IDs for businesses would reduce fraud as it is more challenging to fake a digital identity. This would give businesses the confidence that those they transfer money to are who they claim to be. The IDs would also be used for Know Your Business (KYB) checks, along with ultimate beneficial owners (UBO) checks and comparison to anti-money laundering (AML) databases. If implemented well, this technology could not just reduce financial crime but also allow businesses to save costs on carrying out these checks by conventional methods. Adoption in the financial sector is likely to be strong if made available, as several major FIs are already involved in the project. Regulatory support is also likely as the Financial Conduct Authority (FCA) and the Payment Systems Regulator (PSR) are both involved.

With both these announcements coming at the end of 2024, 2025 is shaping up to be a big year for digital identity in the UK. While it seems unlikely there will be widespread adoption of a digital ID in the UK by consumers before the end of 2025, the foundations for such a success story are being laid. If the Government wants this to happen, targeting key use cases will be essential. Common points of friction for consumers, such as age verification at self-service checkouts, or entry to licensed premises, will play an important role in promoting adoption. It is usual for consumers to have their mobile device on them in such circumstances, so as such, having their ID on that device offers great convenience. It will be the convenience of use and acceptance rate by businesses which ultimately will determine the success of the technology.

A Senior Research Analyst at Juniper Research, Michael primarily conducts research on digital identity and payments markets. His recent reports include Digital Identity, Instant Payments, and Digital Wallets.

Related Research

-

ReportOctober 2025Digital Identity

ReportOctober 2025Digital Identity Louis AtkinDigital Identity Market, 2025-2030

Louis AtkinDigital Identity Market, 2025-2030Juniper Research’s Digital Identity research suite provides a comprehensive and insightful analysis of this market; enabling stakeholders, including digital identity platform providers, digital identity verification providers, government agencies, banks, and many others, to understand future growth, key trends, and the competitive environment.

VIEW -

ReportDecember 2024Digital Identity Verification

ReportDecember 2024Digital Identity Verification Thomas WilsonDigital Identity Verification Market, 2024-2029

Thomas WilsonDigital Identity Verification Market, 2024-2029Our digital identity verification research suite provides detailed analysis of this rapidly changing market; allowing digital identity verification solution providers to gain an understanding of key digital identity trends and challenges, potential growth opportunities, and the competitive environment.

VIEW -

ReportFebruary 2026KYC/KYB Systems

ReportFebruary 2026KYC/KYB Systems Shane O'SullivanKYC/KYB Systems Market, 2026-2030

Shane O'SullivanKYC/KYB Systems Market, 2026-2030Our KYC/KYB Systems research suite provides a detailed and insightful analysis of an evolving market; enabling stakeholders such as financial institutions, eCommerce platforms, regulatory agencies and technology vendors to understand future growth, key trends and the competitive environment.

VIEW

Latest research, whitepapers & press releases

-

ReportMarch 2026Telecoms & Connectivity

ReportMarch 2026Telecoms & Connectivity Alex WebbDirect Carrier Billing Market: 2026-2030

Alex WebbDirect Carrier Billing Market: 2026-2030Our Direct Carrier Billing research suite for mobile network operators provides detailed analysis and strategic recommendations for the direct carrier billing market over the next four years.

VIEW -

ReportMarch 2026Fintech & Payments

ReportMarch 2026Fintech & Payments Lorien CarterCross-border Payments Market: 2026-2030

Lorien CarterCross-border Payments Market: 2026-2030Our Cross-border Payments research suite provides a comprehensive and in-depth analysis of the evolving cross-border payments landscape; enabling stakeholders such as businesses, financial institutions, payment service providers, card networks, regulators, and technology infrastructure providers to understand future growth, key trends, and the competitive environment.

VIEW -

ReportFebruary 2026Telecoms & Connectivity

ReportFebruary 2026Telecoms & Connectivity Ardit BallhysaMobile Messaging Market: 2026-2030

Ardit BallhysaMobile Messaging Market: 2026-2030Juniper Research’s Mobile Messaging research suite provides mobile messaging vendors, mobile network operators, and enterprises with intelligence on how to capitalise on changing market dynamics within the mobile messaging market.

VIEW -

ReportFebruary 2026Fintech & Payments

ReportFebruary 2026Fintech & Payments Shane O'SullivanKYC/KYB Systems Market: 2026-2030

Shane O'SullivanKYC/KYB Systems Market: 2026-2030Our KYC/KYB Systems research suite provides a detailed and insightful analysis of an evolving market; enabling stakeholders such as financial institutions, eCommerce platforms, regulatory agencies and technology vendors to understand future growth, key trends and the competitive environment.

VIEW -

ReportFebruary 2026Telecoms & Connectivity

ReportFebruary 2026Telecoms & Connectivity Molly GatfordRCS for Business Market: 2026-2030

Molly GatfordRCS for Business Market: 2026-2030Our comprehensive RCS for Business research suite provides an in‑depth evaluation of a market poised for rapid expansion over the next five years. It equips stakeholders with clear insight into the most significant opportunities emerging over the next two years.

VIEW -

ReportFebruary 2026Fintech & Payments

ReportFebruary 2026Fintech & Payments Jawad JahanMobile Money in Emerging Markets: 2026-2030

Jawad JahanMobile Money in Emerging Markets: 2026-2030Our Mobile Money in Emerging Markets research report provides detailed evaluation and analysis of the ways in which the mobile financial services space is evolving and developing.

VIEW

-

WhitepaperMarch 2026Telecoms & Connectivity

Alex Webb

WhitepaperMarch 2026Telecoms & Connectivity

Alex WebbDirect Carrier Billing: Unlocking Emerging Revenue Streams for Operators

Our complimentary whitepaper, Direct Carrier Billing: Unlocking Emerging Revenue Streams for Operators, explores the emerging opportunities for mobile network operators to monetise direct carrier billing.

VIEW -

WhitepaperMarch 2026Telecoms & Connectivity

Molly Gatford

WhitepaperMarch 2026Telecoms & Connectivity

Molly GatfordMWC 2026: What's Next for Mobile?

Our latest whitepaper distils the most important announcements from MWC Barcelona 2026 and examines what they mean for the telecoms market over the year ahead. From network APIs and 5G monetisation to AI-RAN, direct-to-cell connectivity, and 5G-Advanced, it explains where the biggest opportunities — and challenges — will emerge next.

VIEW -

WhitepaperMarch 2026Fintech & Payments

Lorien Carter

WhitepaperMarch 2026Fintech & Payments

Lorien CarterThe Transformation of Cross-border Payment Infrastructure

Our complimentary whitepaper, The Transformation of Cross-border Payment Infrastructure, examines the state of the cross-border payments market; explaining the role of key actors in transforming the cross-border payment experience, as well as the current landscape and recent developments within the cross-border payments industry.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

Ardit Ballhysa

WhitepaperFebruary 2026Telecoms & Connectivity

Ardit BallhysaHow Social Media Will Disrupt Mobile Messaging Channels in 2026

Our complimentary whitepaper, How Social Media Will Disrupt Mobile Messaging Channels in 2026, explores the challenges and opportunities for operators and enterprises as social media traffic continues to increase.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

WhitepaperFebruary 2026Telecoms & Connectivity Sam Barker

Sam BarkerProtecting Users from Scam Ads: A Call for Social Media Platform Accountability

In this new whitepaper commissioned by Revolut, Juniper Research examines how scam advertising has become embedded across major social media platforms, quantifies the scale of user exposure and financial harm, and explains why current detection and enforcement measures are failing to keep pace.

VIEW -

WhitepaperFebruary 2026Fintech & Payments

Shane O'Sullivan

WhitepaperFebruary 2026Fintech & Payments

Shane O'SullivanKnow Your Agents (KYA): The Next Frontier in KYC/KYB Systems

Our complimentary whitepaper, Know Your Agents (KYA): The Next Frontier in KYC/KYB Systems, examines the state of the KYC/KYB systems market; considering the impact of regulatory development, emerging risk factors such as identity enabled fraud, and how identity and business verification is evolving beyond traditional customer and merchant onboarding toward agent-level governance.

VIEW

-

Telecoms & Connectivity

Direct Carrier Billing to Grow by $35 Billion Globally Over the Next Four Years, as Anti-fraud Capabilities Are Enhanced by Network APIs

March 2026 -

Fintech & Payments

Sophisticated Microfinance Services Spend to Surpass $22 billion By 2030, as Mobile Money Services in Emerging Markets Mature

March 2026 -

Fintech & Payments

Top Three Global Leaders in Cross-border Payment Infrastructure Revealed

March 2026 -

Telecoms & Connectivity

MVNO Subscriber Revenue to Exceed $50 Billion Globally in 2030

March 2026 -

Fintech & Payments

QUBE Events is excited to bring back the 24th NextGen Payments & RegTech Forum - Switzerland

February 2026 -

Telecoms & Connectivity

OTT Messaging Apps to Exceed 5 Billion Users Globally by 2028; Driving Shift in Enterprise Communication Strategies

February 2026