Capital One Finalises Discover Acquisition: What Does it Mean for Payments?

On Sunday May 18th 2025, Capital One announced that it had finalised the acquisition of Discover Financial Services; completing a drawn-out process which started in February 2024.

This deal, which faced intense regulatory scrutiny, brings together Capital One’s large credit card and financial services business with Discover’s credit card business, Diners Club International brand, PULSE Network, and Discover’s card network; creating the largest credit card issuer, in terms of volume, in the US market. The acquisition came to a total value of $35 billion; representing a massive deal within the payments market in the US.

So, now this massive deal has completed, this blog will explore what the outcome will be – the impact will this have on the wider payments space, and are we going to see fundamental change?

Deal Shakes Up US Credit Card Market

The US credit card market is a highly competitive one, with numerous different players. JPMorgan Chase and American Express have typically been prominent players, but Capital One has also had a strong presence in the market. The US market is a strong mix of high street banks, credit card specialists, digital-only banks, and credit unions, who are all increasingly offering credit cards. Credit cards are high value to banks in terms of revenue, and they allow banks to generate primacy (where they are the main account a customer uses); of high importance in an increasingly congested banking market.

Therefore, in this context, Capital One reinforcing its credit card efforts is a clear strategic move, and will enable it to access a wider part of the market. While the brands are confirmed to be independent to start with, there will likely be consolidation over time; which would create benefits for customers.

Another interesting aspect of this deal is the B2B payments market.

B2B payments is a massive market, with the value of payments globally set to reach $124 billion by 2028, according to our latest data. By expanding its credit card offering, Capital One can move to access this commercial payments area to a much greater degree. Historically, Discover has been focused on the commercial payments space, so this will enable Capital One to leverage Discover’s capabilities to bolster its appeal.

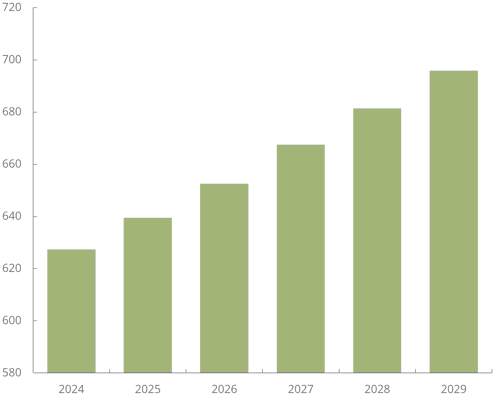

With almost 700 million credit cards being issued globally in 2029, the credit card market is wide beyond the US. By leveraging Discover’s Diners Club brand, which has a strong international component, Capital One will be able to consolidate its international credit cards presence; growing its revenue overall.

All in all, the credit card market will receive a major shake-up, with competition further intensifying.

Credit Cards Issued Globally (m), 2024-2029

Source: Juniper Research

Can Capital One Make Discover a Viable Visa and Mastercard Alternative?

Arguably, the network aspect of Capital One’s purchase of Discover is the most exciting.

Discover offers the Discover Network, PULSE, and Diners Club International, all of which add value to Capital One. PULSE offers strong debit capabilities, across debit cards, ATMs and acceptance. Diners Club is an international credit card brand accepted in over 200 countries and territories. The most interesting element is Discover’s global network. This network operates across the globe and has rising acceptance, supported by an extensive range of partnerships with domestic card schemes such as RuPay (India), mada (Saudi Arabia), and Elo (Brazil).

As such, this network capability gives Capital One a tool it has not had before – its own network on which it can conduct its own transactions, rather than relying on Visa and Mastercard. Indeed, it gives Capital One the opportunity to scale a network to compete with these major players; potentially weakening the duopoly we have seen in the international card network market.

How likely is this to happen? Fundamentally, Discover has struggled to bring its acceptance levels close to Visa and Mastercard’s, so it is still quite a way behind. However, Capital One’s reach and size within the market should give Discover more power to influence merchants into supporting its network. It remains to be seen how extensive Discover’s acceptance will become in the Capital One era, but it is likely to see a boost. We also expect that Capital One will steadily transfer its cards to leverage the Discover network; lowering its costs significantly and giving it more control over its offerings. While this will boost its credit card offering, it will take longer for Discover’s network to close the acceptance gap and break the duopoly.

Is The Era of the Mega Deal Back?

For the past couple of years, fintech and payments have seen readjustments in terms of funding and deals; with many startups seeing reduced valuations in funding rounds in recent times. However, the size of this deal ($35 billion) potentially shows that we are returning to the era of massive deals in the market. Indeed, this has been followed by Global Payments announcing in April 2025 that it was acquiring Worldpay for $24.2 billion; another mega deal.

Fundamentally, competition is rife in payments, and consolidation is a strong force in the market. As market leaders look to better cope with competition from alternative payment methods and new market entrants, consolidation of larger brands is expected to intensify, fuelling future deals.

All in all, Capital One’s deal to acquire Discover is a major one, beyond the large price tag, on the basis that it shakes up the well-established credit cards market; and threatens to compete with Mastercard and Visa.

Over time, we expect Capital One to use its market presence to grow Discover’s network as well as its own credit products; creating a major force within the US payments market. As alternative payments become more important in the US market, we expect greater consolidation. However, as with any merger and acquisition, integration is the biggest challenge. Capital One must work hard to derive value and unlock alignment, in order to take its next step in the market.

Nick Maynard is VP of Fintech Market Research at Juniper Research, enabling clients to size new market opportunities, set priorities for future growth, and understand their customers through survey projects. He also enjoys helping clients promote their expertise and vision of markets with compelling thought‑leadership whitepapers, webinars, and other media.

Related Research

-

ReportJuly 2025Fintech & Payments

ReportJuly 2025Fintech & Payments Michael GreenwoodB2B Payments Market, 2025-2030

Michael GreenwoodB2B Payments Market, 2025-2030Juniper Research’s B2B Payments research suite provides a comprehensive and insightful analysis of this market; enabling stakeholders from B2B payment platform providers to regulators and banks, to understand future growth, key trends and the competitive environment.

VIEW -

ReportAugust 2024Fintech & Payments

ReportAugust 2024Fintech & Payments Nick MaynardPayment Card Technologies Market, 2024-2029

Nick MaynardPayment Card Technologies Market, 2024-2029Our Payment Card Technologies research report provides a detailed evaluation and analysis of the ways in which the payment card is changing; impacting the wider payments industry.

VIEW

Latest research, whitepapers & press releases

-

ReportMarch 2026Fintech & Payments

ReportMarch 2026Fintech & Payments Lorien CarterCross-border Payments Market: 2026-2030

Lorien CarterCross-border Payments Market: 2026-2030Our Cross-border Payments research suite provides a comprehensive and in-depth analysis of the evolving cross-border payments landscape; enabling stakeholders such as businesses, financial institutions, payment service providers, card networks, regulators, and technology infrastructure providers to understand future growth, key trends, and the competitive environment.

VIEW -

ReportFebruary 2026Telecoms & Connectivity

ReportFebruary 2026Telecoms & Connectivity Ardit BallhysaMobile Messaging Market: 2026-2030

Ardit BallhysaMobile Messaging Market: 2026-2030Juniper Research’s Mobile Messaging research suite provides mobile messaging vendors, mobile network operators, and enterprises with intelligence on how to capitalise on changing market dynamics within the mobile messaging market.

VIEW -

ReportFebruary 2026Fintech & Payments

ReportFebruary 2026Fintech & Payments Shane O'SullivanKYC/KYB Systems Market: 2026-2030

Shane O'SullivanKYC/KYB Systems Market: 2026-2030Our KYC/KYB Systems research suite provides a detailed and insightful analysis of an evolving market; enabling stakeholders such as financial institutions, eCommerce platforms, regulatory agencies and technology vendors to understand future growth, key trends and the competitive environment.

VIEW -

ReportFebruary 2026Telecoms & Connectivity

ReportFebruary 2026Telecoms & Connectivity Molly GatfordRCS for Business Market: 2026-2030

Molly GatfordRCS for Business Market: 2026-2030Our comprehensive RCS for Business research suite provides an in‑depth evaluation of a market poised for rapid expansion over the next five years. It equips stakeholders with clear insight into the most significant opportunities emerging over the next two years.

VIEW -

ReportFebruary 2026Fintech & Payments

ReportFebruary 2026Fintech & Payments Jawad JahanMobile Money in Emerging Markets: 2026-2030

Jawad JahanMobile Money in Emerging Markets: 2026-2030Our Mobile Money in Emerging Markets research report provides detailed evaluation and analysis of the ways in which the mobile financial services space is evolving and developing.

VIEW -

ReportJanuary 2026IoT & Emerging Technology

ReportJanuary 2026IoT & Emerging Technology Louis AtkinPost-quantum Cryptography Market: 2026-2035

Louis AtkinPost-quantum Cryptography Market: 2026-2035Juniper Research’s Post-quantum Cryptography (PQC) research suite provides a comprehensive and insightful analysis of this market; enabling stakeholders, including PQC-enabled platform providers, specialists, cybersecurity consultancies, and many others, to understand future growth, key trends, and the competitive environment.

VIEW

-

WhitepaperMarch 2026Telecoms & Connectivity

Molly Gatford

WhitepaperMarch 2026Telecoms & Connectivity

Molly GatfordMWC 2026: What's Next for Mobile?

Our latest whitepaper distils the most important announcements from MWC Barcelona 2026 and examines what they mean for the telecoms market over the year ahead. From network APIs and 5G monetisation to AI-RAN, direct-to-cell connectivity, and 5G-Advanced, it explains where the biggest opportunities — and challenges — will emerge next.

VIEW -

WhitepaperMarch 2026Fintech & Payments

Lorien Carter

WhitepaperMarch 2026Fintech & Payments

Lorien CarterThe Transformation of Cross-border Payment Infrastructure

Our complimentary whitepaper, The Transformation of Cross-border Payment Infrastructure, examines the state of the cross-border payments market; explaining the role of key actors in transforming the cross-border payment experience, as well as the current landscape and recent developments within the cross-border payments industry.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

Ardit Ballhysa

WhitepaperFebruary 2026Telecoms & Connectivity

Ardit BallhysaHow Social Media Will Disrupt Mobile Messaging Channels in 2026

Our complimentary whitepaper, How Social Media Will Disrupt Mobile Messaging Channels in 2026, explores the challenges and opportunities for operators and enterprises as social media traffic continues to increase.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

WhitepaperFebruary 2026Telecoms & Connectivity Sam Barker

Sam BarkerProtecting Users from Scam Ads: A Call for Social Media Platform Accountability

In this new whitepaper commissioned by Revolut, Juniper Research examines how scam advertising has become embedded across major social media platforms, quantifies the scale of user exposure and financial harm, and explains why current detection and enforcement measures are failing to keep pace.

VIEW -

WhitepaperFebruary 2026Fintech & Payments

Shane O'Sullivan

WhitepaperFebruary 2026Fintech & Payments

Shane O'SullivanKnow Your Agents (KYA): The Next Frontier in KYC/KYB Systems

Our complimentary whitepaper, Know Your Agents (KYA): The Next Frontier in KYC/KYB Systems, examines the state of the KYC/KYB systems market; considering the impact of regulatory development, emerging risk factors such as identity enabled fraud, and how identity and business verification is evolving beyond traditional customer and merchant onboarding toward agent-level governance.

VIEW -

WhitepaperFebruary 2026Telecoms & Connectivity

Molly Gatford

WhitepaperFebruary 2026Telecoms & Connectivity

Molly Gatford3 Key Strategies for Capitalising on RCS Growth in 2026

Our complimentary whitepaper, 3 Key Strategies for Capitalising on RCS Growth in 2026, explores key trends shaping the RCS for Business market and outlines how mobile operators and platforms can accelerate adoption and maximise revenue over the next 12 months.

VIEW

-

Fintech & Payments

Sophisticated Microfinance Services Spend to Surpass $22 billion By 2030, as Mobile Money Services in Emerging Markets Mature

March 2026 -

Fintech & Payments

Top Three Global Leaders in Cross-border Payment Infrastructure Revealed

March 2026 -

Telecoms & Connectivity

MVNO Subscriber Revenue to Exceed $50 Billion Globally in 2030

March 2026 -

Fintech & Payments

QUBE Events is excited to bring back the 24th NextGen Payments & RegTech Forum - Switzerland

February 2026 -

Telecoms & Connectivity

OTT Messaging Apps to Exceed 5 Billion Users Globally by 2028; Driving Shift in Enterprise Communication Strategies

February 2026 -

Fintech & Payments

Calling All Fintech & Payment Innovators: Future Digital Awards Now Open for 2026

February 2026